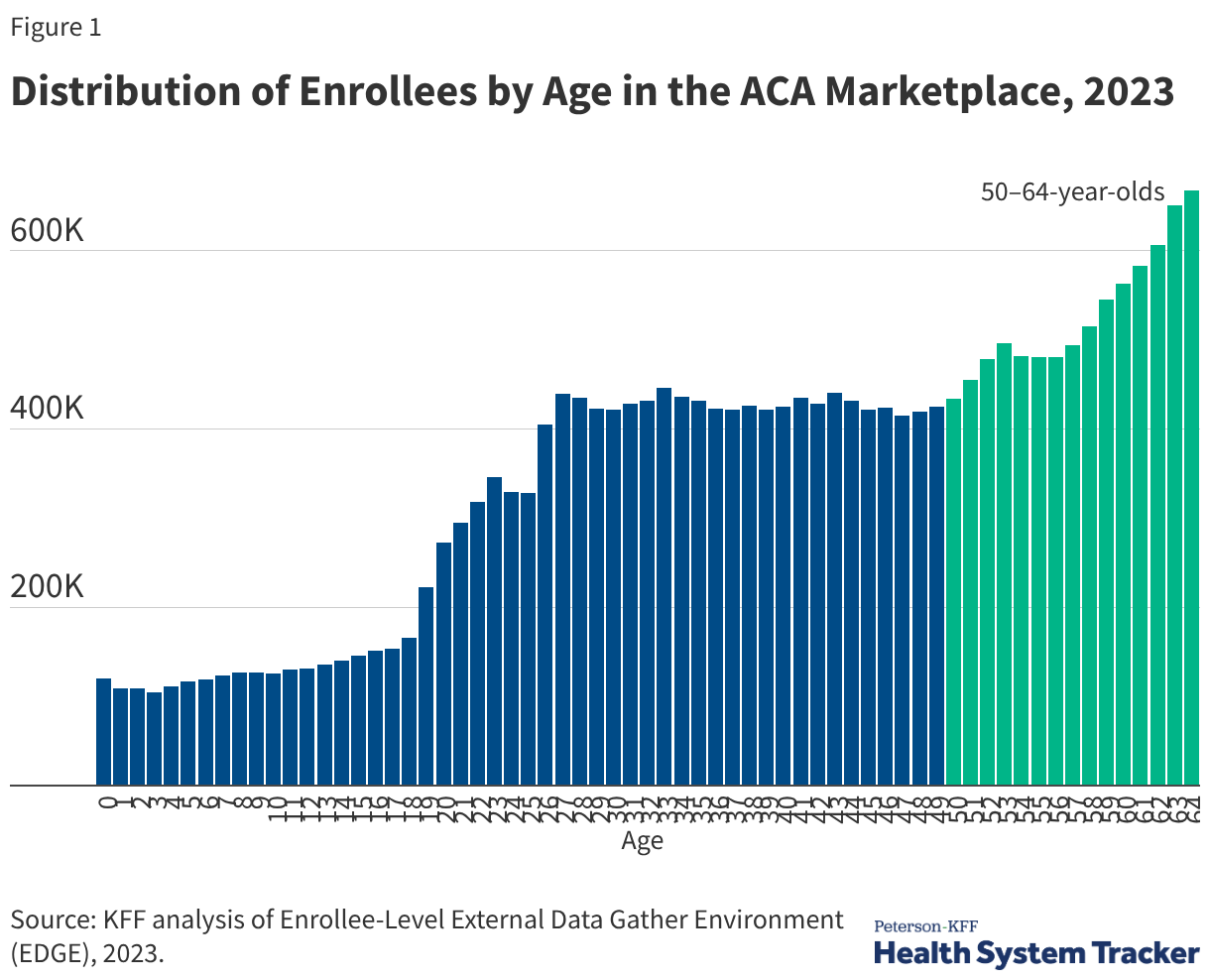

With the expiration of the Affordable Care Act (ACA) Marketplace’s enhanced premium tax credits as of December 31, 2025, the average ACA enrollee who received a premium tax credit faces a doubling of their premium payments for the same plan. Older adults, who make up a large share of Marketplace enrollees, are disproportionately affected by the loss of enhanced premium tax credits. About one-third of all Marketplace enrollees (8 million people) were between ages 50 and 64 in 2023 (the most recent year of data available), constituting a sizeable portion of those purchasing Marketplace plans. The number of people with ACA Marketplace coverage generally increases with age, peaking at age 64, as the chart below shows.

Marketplace enrollees between the ages of 50 and 64 are disproportionately affected by the expiration of the enhanced premium tax credits, not just because they make up a large number of Marketplace enrollees, but also because the cost of Marketplace premiums tend to rise with age. Older ACA enrollees with annual incomes just above 400% of the federal poverty line (FPL) are expected to see the largest increases in premium payments. Older adults also make up a relatively large share of ACA Marketplace enrollees with incomes above 400% FPL, who will no longer be eligible for any assistance with the expiration of the enhanced premium subsidies.

Why do older adults purchase ACA Marketplace plans?

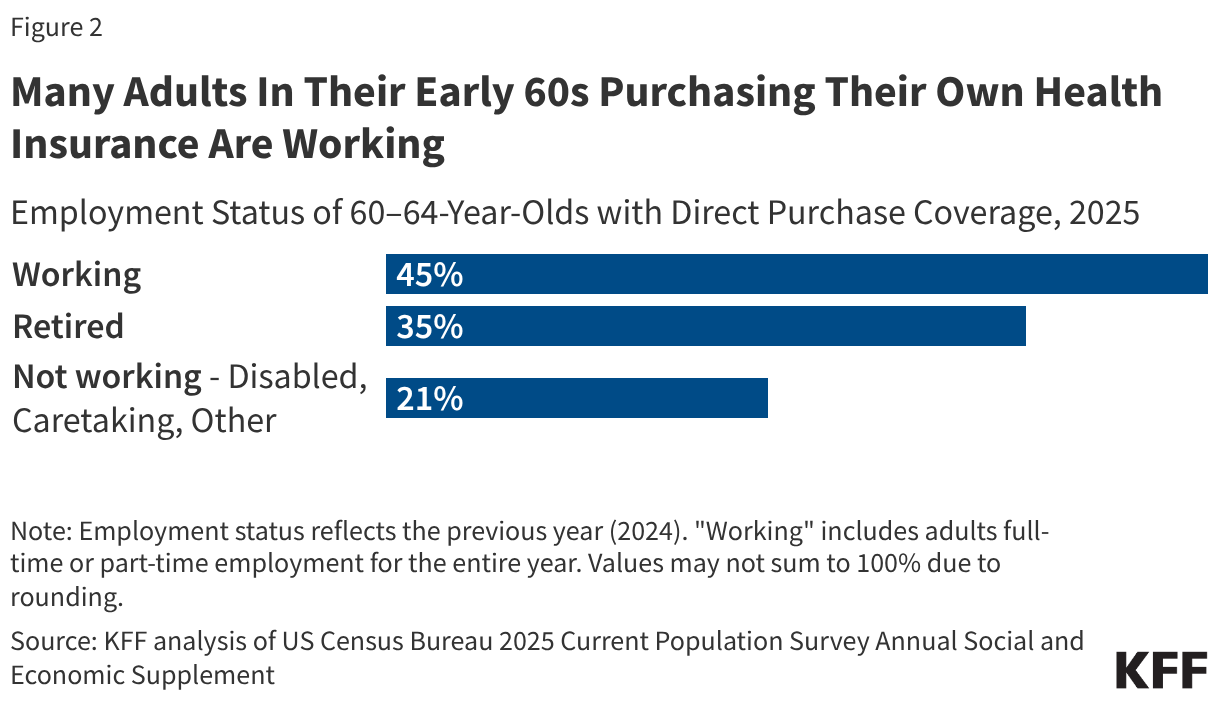

People in their late 50s and early 60s rely on the ACA Marketplace for health insurance coverage for a variety of reasons. Across all ages, most Marketplace enrollees are working, but they often work in fields that frequently do not offer employer health insurance, are self-employed, or own or work at small businesses. Among direct purchase insurance enrollees in their early 60s, nearly half (45%) are working full or part time, but about a third (35%) are retired, and 21% are not working because of a disability, have caregiving responsibilities, or other reasons.

While people in the U.S. have been retiring at later ages in recent years, on average, many people retire earlier than expected and often do so involuntarily (e.g., because they are too sick to work, can no longer do physically demanding work, or were laid off and could not find new employment). A survey by the Employee Benefit Research Institute found that most people who retire early do so for reasons beyond their control, while two in five retired early because they felt they could afford to do so.

As the number and share of employers offering retiree health benefits to pre-Medicare retirees continues to shrink, fewer people who leave the workforce before age 65 have access to retiree health benefits through their former employers. In 2025, only 27% of large firms (with 200 or more workers) that offered health benefits also provided retiree coverage to at least some employees under age 65. For older adults without access to an employer-based plan, ACA coverage may be their only insurance option until they become eligible for Medicare at age 65.

Why have older adults been disproportionately impacted by the expiration of enhanced premium tax credits?

Across all ages, on average, premium payments for subsidized enrollees are estimated to have more than doubled in 2026 for enrollees wanting to keep the same plan, rising an average of 114%, because of the expiration of the enhanced premium tax credits. However, some enrollees could have switched to a plan with a lower premium but higher deductible to lessen their premium payment increases. Around nine in 10 ACA enrollees have annual incomes less than 400% FPL and will therefore continue to receive some tax credit without the enhanced tax credits, but at a lower level of federal financial assistance; most enrollees over age 50 will likely continue to receive tax credits.

However, older, middle- and upper-income ACA enrollees are disproportionately affected by the spike in premium payments. This is for three main reasons. First, people ages 50-64 make up about half of individual market enrollees with incomes above 400% FPL, meaning they will not be eligible for any federal financial assistance without the enhanced premium tax credits. Second, because premiums in the ACA marketplace are higher for older than younger adults, this group faces unsubsidized premiums that are up to three times higher than for younger enrollees. In 2026, unsubsidized benchmark premiums increased by 26% on average, the largest increase in eight years, driven in part by an expectation that healthier enrollees would drop coverage as the enhanced tax credits expire. As a result, older, middle- and upper-income enrollees faced a “double whammy” of both the loss of all federal premium financial assistance and an increase in the cost of unsubsidized premiums that is larger than other age groups.

Third, many ACA enrollees in their 50s and early 60s were already signed up for one of the lowest-premium plans available to them and therefore had limited options to switch to a lower-premium plan for the 2026 plan year. Of ACA Marketplace enrollees aged 50-64 not receiving cost-sharing reductions (and therefore likely with incomes over 250% of poverty), most (64%) were already enrolled in a bronze plan, 22% were in a gold plan, and just 13% were in a silver plan for the 2023 plan year. Those in a silver or gold plan in 2025 could have switched to a bronze plan for 2026 to mitigate the increase in premium payments but would then have a deductible much higher than their previous plan.

For 2026 health coverage, the average gold plan deductible is $1,722, the average silver plan deductible (without cost-sharing assistance) is $5,304, and the average bronze plan deductible is $7,476.

How much have premium payments increased for older ACA enrollees, now that enhanced tax credits expired?

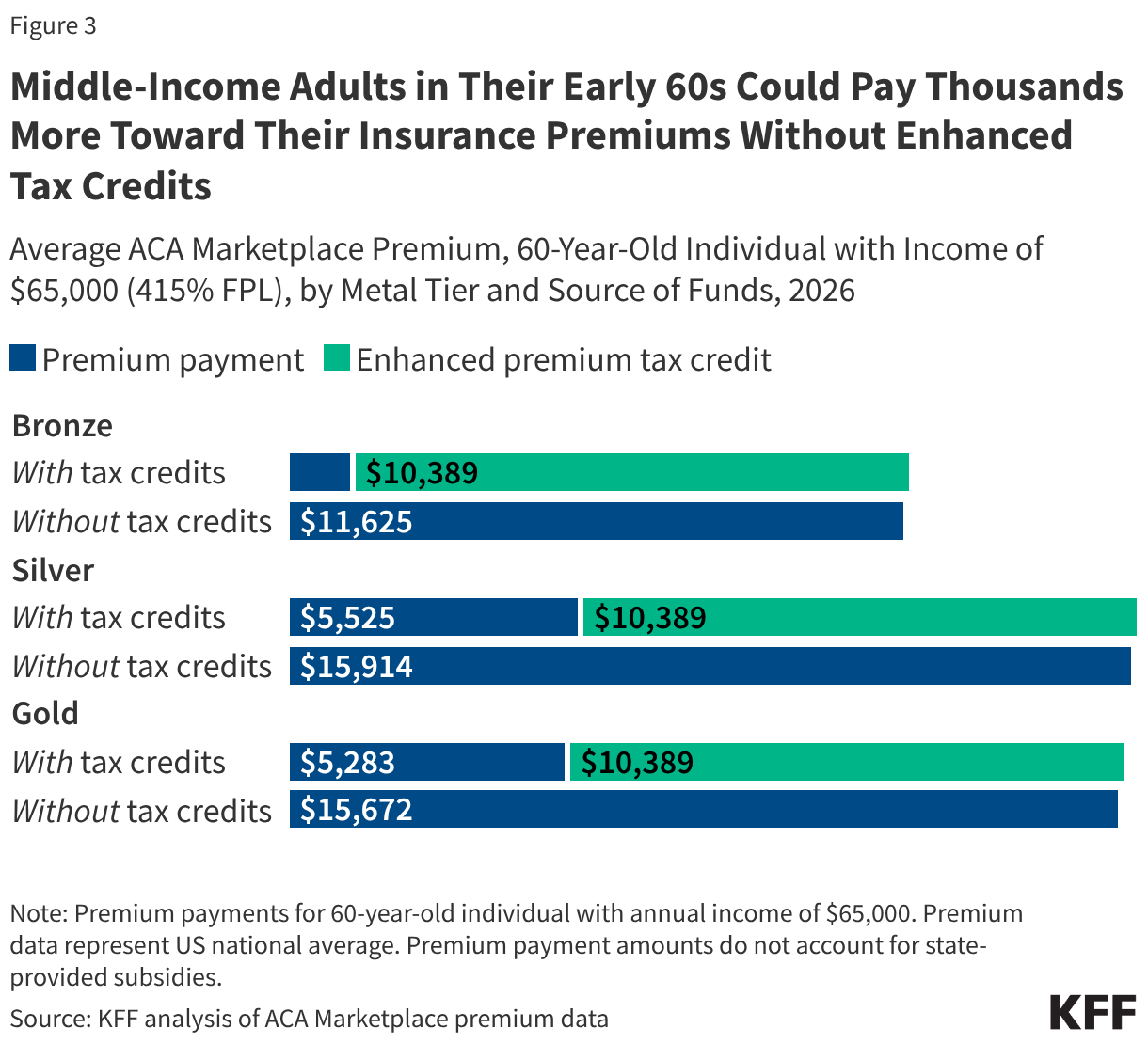

On average, a 60-year-old with an income of $65,000 (just over four times the poverty level) pays $10,389 more annually ($865 per month) toward their premium now that enhanced premium tax credits have expired.

The national average annual unsubsidized premium payment for a 60-year-old in 2026 is $11,625 for the lowest-cost bronze plan, $15,914 for the benchmark silver plan, and $15,672 for the lowest-cost gold plan. (Due to “silver loading” unsubsidized silver plans are often priced similarly to gold, which is why few middle- or higher-income people, who are ineligible for cost-sharing reductions, are enrolled in silver plans).

On average, with enhanced premium tax credits, a 60-year-old spent 2% of their annual income of $65,000 on a bronze plan. However, without enhanced premium tax credits, the average bronze plan costs the same 60-year-old 18% of their annual income. Similarly, with enhanced premium tax credits, the average silver and gold plan would each cost a 60-year-old making $65,000 per year about 8.5% of their income. However, with the expiration of the enhanced premium tax credits, the average silver and gold plan would now cost nearly one-quarter (24%) of the same 60-year-old’s annual income.

Depending on location, some older enrollees could expect to pay less or more. The average annual unsubsidized 2026 premium for the lowest-cost bronze plan for a 60-year-old is highest in Wyoming ($20,005), West Virginia ($19,747), and Alaska ($17,045). By contrast, Maryland ($7,215), New York ($7,318), and Massachusetts ($8,002) have the lowest average unsubsidized bronze premiums for a 60-year-old.

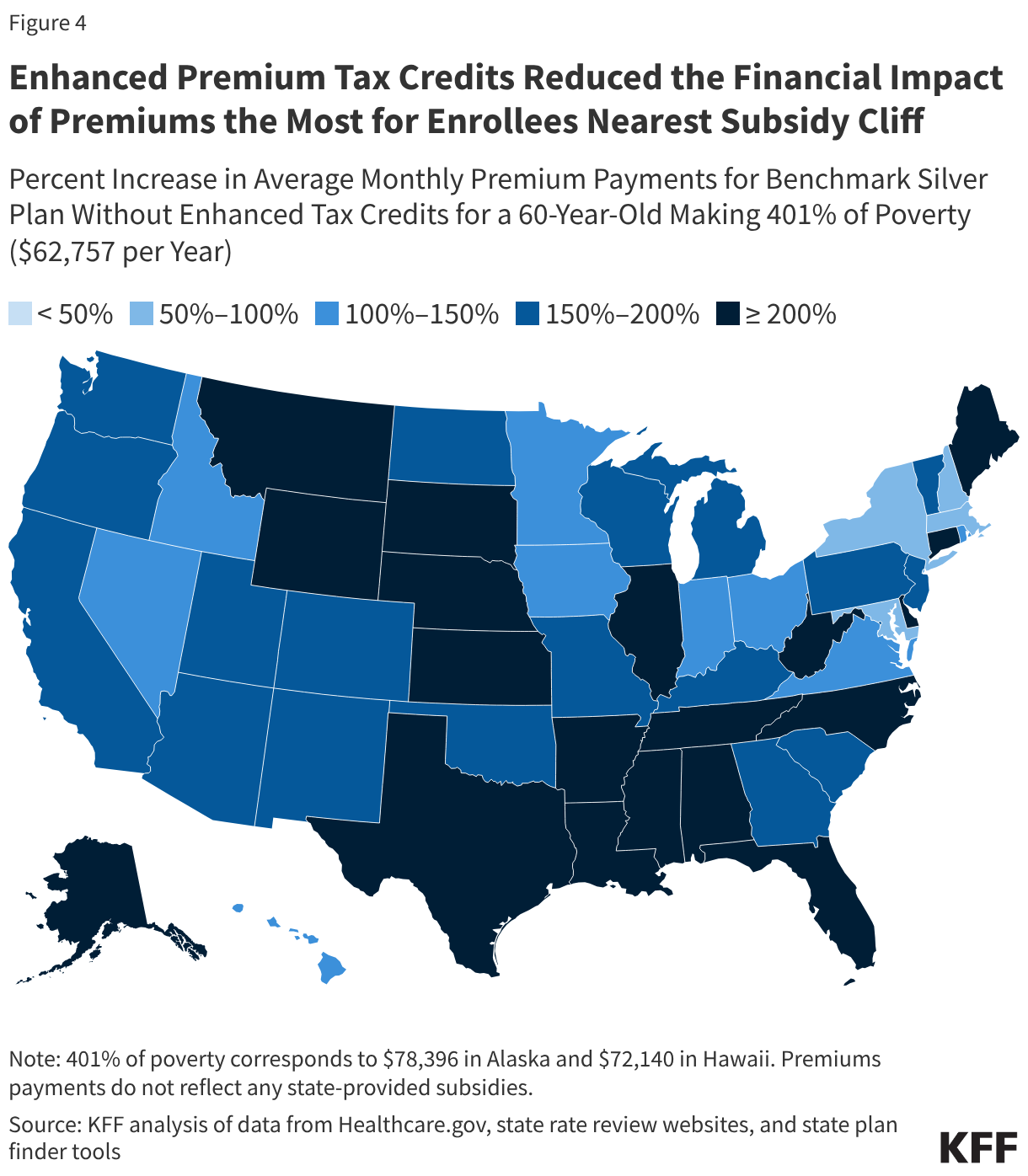

An annual income at 401% FPL represents an annual salary of $62,757 for an individual in the contiguous United States. Because the cost of living is higher in Alaska and Hawaii, 401% of federal poverty is $78,396 and $72,140 for individuals there, respectively. In 46 states and the District of Columbia, a 60-year-old at 401% of poverty will see their average annual premium payment for a benchmark silver plan at least double without enhanced tax credits.

As seen in Figure 4, in 19 states, this person would see their premium payment at least triple on average for a benchmark silver plan, consuming more than 25% of annual income. States with the highest premium payment increases due to expired enhanced tax credits for a 60-year-old at 401% of poverty purchasing a benchmark silver plan are Wyoming ($22,452 increase per year), West Virginia ($22,006), and Alaska ($19,636). The smallest increases caused by the loss of enhanced tax credits for what enrollees pay annually for the benchmark silver plan are in New York ($4,469), Massachusetts ($4,728) and New Hampshire ($4,877).

Methods

Age of ACA Marketplace enrollees was obtained using the 2023 Enrollee Data Gathering Environment (EDGE) Limited Data Set from CMS. Enrollees were restricted to those whose longest enrollment during the year was in an on-exchange individual plan. When determining whether enrollees received cost-sharing reductions, the longest enrollment during the year was considered. Employment status by age and income come from the 2025 Current Population Survey Annual Social and Economic Supplement (ASEC). Those with direct purchase insurance exclude respondents age 65 or older and are dually insured with employer-sponsored coverage, Medicaid, or Medicare. Insurance status refers to current year and employment status pertains to the full preceding year. Retired individuals may have worked for part of the year; working includes full- and part-time employment for the entire year.

This work was supported in part by the John A. Hartford Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.