State Farm reported an underwriting gain of $1.5 billion for its property/casualty businesses in 2025, representing a turnaround from an underwriting loss of more than $6 billion in 2024—and more than $10 billion of underwriting losses in each of the two prior years.

While the overall return to profitability prompted State Farm to announce a $5 billion payout of dividends to policyholders, the giant personal lines insurer’s homeowners underwriting results were still written in red ink.

Related: State Farm Mutual to Pay $5B Dividend to Auto Insurance Customers

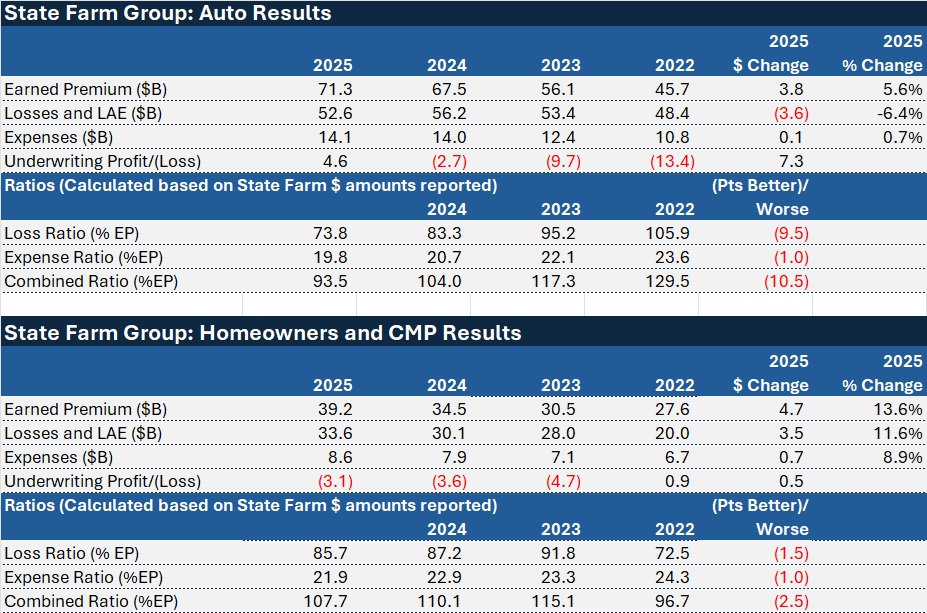

State Farm’s auto underwriting results drove the overall improvement. With auto earned premiums jumping nearly 6% to $71.3 billion, State Farm’s auto underwriting profit approached $5 billion. The actual reported figure, $4.6 billion, translates to a combined ratio of 93.5—more than 10 points better than 2024’s auto combined ratio of roughly 104.

Property was a different story. Even though earned premiums for homeowners and commercial multiple peril policies jumped more than 13% for the second straight year, State Farm’s property combined ratio neared 108, only 2.5 points better than 2024.

State Farm’s media statement reporting 2025 financial results highlights the impact of the January 2025 Los Angeles wildfires on last year’s home insurance underwriting results.

“More than 1,000 State Farm employees, agents and agent team members deployed to California to help more than 13,500 customers with claims following devastating wildfires in January 2025. To date, State Farm Mutual and State Farm General Insurance Company together have issued over $5 billion in payments to families whose cars, homes and property were damaged or destroyed by those fires,” the statement said, adding that the total could reach $7 billion when claims, repairs and rebuilds still underway are ultimately completed.

“Hundreds of State Farm team members remain on the ground in the Los Angeles area assisting customers,” the statement said.

Across the nation, State Farm Mutual and its P/C affiliates reported incurred claims of $78 billion in 2025, including payments of nearly $15 billion for catastrophes, the statement notes. Incurred losses plus loss adjustment expenses were more than $86 billion based on the separately disclosed figures for auto and property included in the report.

In total, State Farm said that its P/C insurance companies reported a combined underwriting profit of $1.5 billion on earned premium of $111.6 billion. The 2025 underwriting gain, combined with investment and other income of $7.0 billion, resulted in a P/C pre-tax operating profit of $8.5 billion, compared to an operating loss of $111 million in 2024 (and operating losses of more than $8 billion in each of the prior two years).

Total revenue, which includes premium revenue, earned investment income and realized capital gains and losses was $132.3 billion for 2025, up 7.5% from $123.0 billion for 2024.

On the bottom line, State Farm reported a net income figure of $12.9 billion in 2025, more than double the $5.3 billion figure recorded in 2024. Reported net income for 2025 includes the impact of $2.0 billion of realized capital gains, net of tax.

The net worth for State Farm Mutual at year-end 2025 was $170 billion, compared to $145.2 billion at year-end 2024. This increase was mainly the result of operating profit from the P/C affiliates and increased values of the P/C companies’ unaffiliated stock portfolios.

“Although financial information is presented on a group/line of business basis, State Farm Mutual Automobile Insurance Company and each of its affiliates must meet solvency and regulatory requirements on an individual entity-by-entity basis without regard to the solvency or financial condition of any other affiliated entity,” a footnote to the report says.

This footnote is not new. It has been included at the bottom of prior financial reports from State Farm but seemed to take on added significance last year as State Farm leaders fought for California homeowners insurance rate increases, highlighting the precarious financial condition of one affiliated entity—State Farm’s California homeowners insurance company, State Farm General—to support its requests for approval of higher rates.

Related: S&P Puts State Farm General Ratings on CreditWatch | LA Fire-Related Capital Hit Prompts State Farm Emergency Rate Request

Beyond P/C

The State Farm Group’s insurance operations consist of 14 P/C insurance companies and two life companies.

In addition to the $5 billion in payments to auto customers, State Farm Life Insurance Company and State Farm Life and Accident Assurance Company reported nearly $1 billion ($924 million) in total dividends to qualified life policyholders— the highest in those companies’ history, according to State Farm’s media statement.

The two life companies reported premium income of $6.9 billion and net income for 2025 was $2.1 billion, with $1.2 trillion in individual life insurance in force at the end of 2025.

State Farm Mutual also reported an underwriting loss of $189 million for individual health insurance operations on net written premium of $756 million.

State Farm’s investment Planning Services operation reported at net loss of $39 million in 2025, with total assets under management of $17.5 billion.

Auto Improvement vs. Competitors

Highlighting the positive performance in the auto business led State Farm Mutual Automobile Insurance Company, State Farm said the one-time $5 billion cash back dividend for qualifying auto customers came on top of auto rate reductions which netted customers some $4.6 billion in lower annual premiums across 40 states.

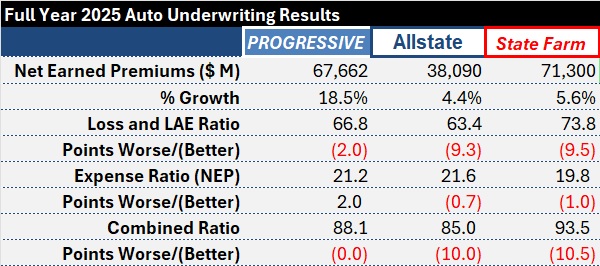

The improvement in State Farm’s P/C businesses—a nearly 10-point drop in its loss and loss adjustment ratio—was on par with one of its competitors, Allstate, and larger than a two-point improvement for Progressive.

All three carriers reported improved underwriting results, but State Farm’s personal auto loss and LAE ratio, at 73.8, remains higher than the mid-60s loss and LAE ratios reported by Progressive and Allstate.

According to figures compiled by Carrier Management from financial reports of all three carriers, State Farm and Allstate reported lower growth in auto earned premiums than Progressive in 2025. Progressive’s earned premiums jumped nearly 19% last year, coming in at more than three-times the 5.6% jump in auto earned premiums reported by State Farm.

Topics

Profit Loss

Underwriting

State Farm