Wildfires, severe convective storms and floods — also known as secondary perils — accounted for a record 92% of total global natural catastrophe insured losses of US$107 billion in 2025, according to Swiss Re Institute.

Wildfires set a new loss record after the Palisades and Eaton fires in Los Angeles in January 2025 created combined insured losses of US$40 billion, while losses from severe convective storms (SCS) — which include hailstorms and damaging winds — were elevated at US$51 billion in 2025, said Swiss Re. Swiss Re noted that 2025 was the third costliest year on record for SCS after 2023 and 2024 (in 2025 prices).

Wildfire stands out as the fastest-growing risk, with insured losses increasing by an estimated 12% per year, said the Swiss Re sigma report titled “Natural catastrophes in 2025: the persistent rise of wildfire and storm risk.”

Meanwhile, global flood-related insured losses were well below average in 2025 – at US$3.4 billion compared to a US$15.4 billion previous five-year average, the report said.

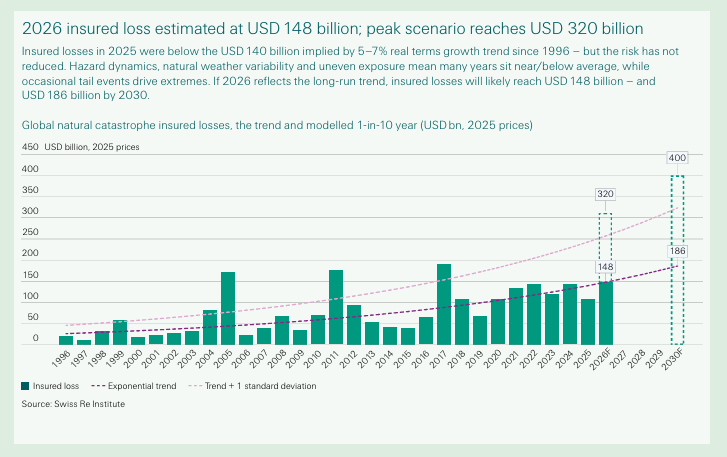

“While US$107 billion is high by historical standards, it was well below the US$140 billion implied by the long-term growth trend due to the absence of a major US hurricane landfall,” Swiss Re added.

Despite one below-trend year in 2025, “insured losses are still rising by 5%‒7% annually on average in real terms,” the report said.

“The below-trend natural catastrophe losses seen in 2025 are the result of favourable variability rather than any easing of underlying risk. If losses return to normal long-term levels, they would total US$148 billion in 2026,” commented to Balz Grollimund, head Catastrophe Perils, in a statement accompanying the report.

The report warned that insured losses from natural disasters will likely reach US$186 billion by 2030, if losses return to long-term trends.

“According to our modeled peak-loss scenario, insured losses could even climb to about US$320 billion in 2026. As exposure keeps building, the upward trend in insured losses is structural and it is critical to identify the risk drivers behind this to manage and reduce risks before losses occur,” Grollimund continued.

Insurance Protection Gaps

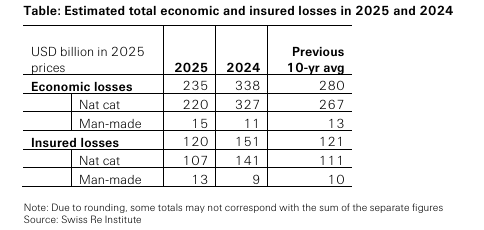

Global economic losses from natural catastrophes were US$220 billion in 2025, about 49% of which were insured — the highest insured share on sigma records. (Economic losses include insured and uninsured losses. Protection gaps are the share of uninsured losses relative to total economic losses).

Man-made insured losses during 2025 were US$13 billion with man-made economic losses of US$15 billion.

Discussing the record percentage of economic losses that were insured last year, Swiss Re said the fact that the figure hit almost 50% is a clear indication that the insurance industry is playing its part in closing global insurance protection gaps.

“However, protection gaps remain especially wide in emerging economies, where 80–90% of catastrophe losses are typically not covered by insurance, underscoring the need to pair stronger adaptation and risk management with broader, more accessible insurance coverage,” the report said.

The report noted that even major advanced economies face significant underinsurance for low-frequency high-impact events such as earthquakes.

Swiss Re said adaptation measures can help stabilize the loss trajectory and ease some of the cost pressures. “For example, in the U.S., where catastrophe losses are now the largest share of personal property insurance claims, targeted physical adaptation at homeowner level can reduce insured losses.”

The report said natural catastrophe protection gaps can be narrowed by taking an integrated approach “that combines insurance coverage with risk-adaptation measures in exposed areas…”

Editor’s note: So-called secondary perils include wildfires, SCS, floods, winter storms (outside of Europe), droughts and all other non-primary natural catastrophe perils. However, secondary perils exclude earthquakes, tropical cyclones and extratropical cyclones (European winter storms).

Photograph: A firefighter battles the Palisades Fire as it burns a structure in the Pacific Palisades neighborhood of Los Angeles, Jan. 7, 2025. (AP Photo/Ethan Swope,File)

Topics

Catastrophe

Natural Disasters

Profit Loss

Flood

Wildfire

Windstorm

Interested in Catastrophe?

Get automatic alerts for this topic.