The current administration is placing a new emphasis on potential fraud in Medicaid. The Centers for Medicare and Medicaid Services (CMS’) current efforts are focused on Minnesota and three other states with Democratic governors (California, Maine, and New York). The House Committee on Energy and Commerce has also sent requests for information about potential Medicaid fraud to 11 states (the 4 CMS is focused on and 7 others, including 2 with Republican governors). CMS has historically partnered with states to identify and resolve issues of fraud, waste, and abuse, and denied the federal share of Medicaid spending when fraud has been identified by an audit, investigation, or reported by the state. However, CMS has recently announced a new approach to fraud that will rely more heavily on options to pause or withhold significant amounts of federal funding in cases of potential fraud, which could have broad implications for states and enrollees. This issue brief explains the new approach. Key findings include:

- CMS’ historic practice has relied on disallowing federal Medicaid payments when fraud is identified (typically through an audit), a process that may take several years to implement.

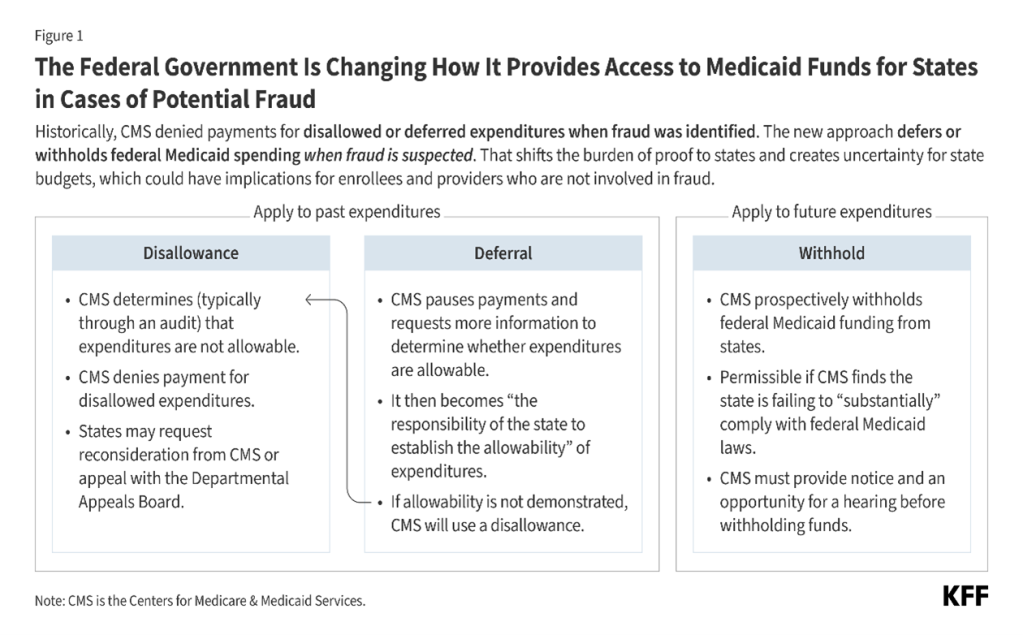

- CMS’ new approach to potential fraud involves deferring and withholding federal Medicaid payments when fraud is suspected (Figure 1). This approach differs from prior approaches because it can have more immediate consequences, may place a much larger share of federal spending at risk (including spending that pays for services uninvolved in fraud), and proactively shifts the burden of proof to states to obtain federal funds.

- While all approaches aim to limit future fraudulent payments using tools such as corrective action plans, the new approach to federal Medicaid spending when fraud is suspected creates uncertainty for state budgets and could have implications for Medicaid enrollees and providers who are not involved in fraud.

What is a disallowance?

The federal and state governments share responsibility for financing Medicaid, and states draw on federal funds to pay health care providers and health plans for providing health care to enrollees. The federal government makes quarterly grant awards to states to cover the federal share of Medicaid spending. Awards reflect states’ estimated expenditures for the upcoming quarter and adjustments from prior quarters’ expenses. Adjustments reflect various considerations such as:

- Instances where states’ estimated expenditures are higher or lower than actual expenditures

- Changes to accounting practices or federal matching rates

- Reductions in payment resulting from claims where fraud has been identified

Publicly-available data on Medicaid expenditures show the total amount of adjustments each year, reflecting the net impact of all various factors, and do not specifically identify adjustments due to disallowances and deferrals.

Historically, CMS has used disallowances to deny federal matching funds for prior state Medicaid expenditures that are determined to be not allowable. There is limited information available about the frequency and scope of Medicaid disallowances, but an older report by the Government Accountability Office (GAO) suggests that they were not infrequent between 2014 and 2017. Upon receiving a disallowance notice, states may request that CMS reconsider the decision and provide additional information to CMS to demonstrate that the expenditures were allowable or proceed with settling the disallowance. In all cases, once CMS has issued a disallowance, “the state has the burden of documenting the allowability” of the expenditures to overturn the disallowance. When states request a reconsideration, CMS has 60 days to decide, although this timeline may take longer if CMS requests additional information from the state.

States may appeal the disallowance decisions to a Departmental Appeals Board, but the state still has the burden of proof for documenting the allowability of expenditures and the process may take years to resolve. More information is publicly available for cases where states do appeal the decisions than for cases where they settle or request a reconsideration. In such cases, data about the decisions of the Department Appeals Board are available online through the Department’s website. Between 2020 and 2025, the Departmental Appeals Board has issued 12 Medicaid disallowance rulings (with 6 rulings being an appeal of a prior case). In all 6 new rulings, there were on average 15 years between the oldest year of disputed expenditures and the final ruling, highlighting how long it takes to resolve these cases (see Figure 2 for an example from Texas). All cases were decided in favor of CMS.

The amount of disputed disallowances where the Departmental Appeals Board issued a ruling between 2020 and 2025 ranged from less than $500,000 to almost $200 million, but these amounts reflect differences in the number of years and scope of services within the disallowed claims. Some of the largest disallowances to be upheld involve disproportionate share hospital (DSH) payments.

- The largest disallowance ruling between 2020 and 2025 was $195.7 million in a case involving Michigan’s DSH payments between 2001-2009. In that instance, CMS in 2018 determined that the state had made DSH payments to a small number of hospitals that were ineligible to receive them. The Departmental Appeals Board ruling was in 2024.

- The second largest disallowance ruling between 2020 and 2025 was for more than $97 million in a case where Florida made DSH payments between 2006-2013 in excess of the limits established for specific hospitals (CMS first issued this disallowance in 2016 and the Departmental Appeals Board ruling was in 2021).

What is a deferral?

With deferrals, CMS pauses payment for prior state Medicaid expenditures and requires the state to provide additional information demonstrating that expenditures are “allowable.” Deferrals may be initiated by either federal or state governments and may be used to pause federal funding while the state and federal governments work out the details of a disallowance, and in cases where fraud, waste, or abuse has been identified and the state and federal governments are gauging the extent of the issue. In the past, deferrals were used as temporary measures that pause funding until CMS either reimburses the expenditures or issues a disallowance. Deferral notices must specify the reason for the deferral and include a request for all documents and materials that CMS believes are necessary to determine whether the expenses are allowable.

After receiving a deferral notice from CMS, states have 60 days to provide all requested documents and materials unless they request an additional 60-day extension. CMS usually begins document review within 30 days but may request different formats or additional materials from the state. States have 15 days to submit additional materials and if they do not meet that deadline, CMS disallows the expenses. Once all documents are available, CMS has 90 days to review and determine whether expenditures are allowable. If CMS determines expenditures are not allowable, the disallowance process begins.

Deferrals are receiving new attention after CMS announced that it would temporarily defer $259 million in federal Medicaid payments to Minnesota for claims paid in fiscal year (FY) 2025, an unprecedentedly large amount. In the announcement, CMS noted that it may continue to defer federal payments, and that similar announcements for other states would likely be coming soon. As of March 16, 2026, 3 additional states have received formal letters from CMS requesting information about program integrity, and 11 states have received formal letters from the House Committee on Energy and Commerce (Figure 3).

What is a withhold?

In January 2026, CMS notified Minnesota that pending the outcome of a hearing, it would begin withholding $515 million in quarterly federal Medicaid payments moving forward, a process that has seldom been used in prior years. Withholding funds has been referred to as the “compliance process” because it is only permissible in cases where the state is failing to comply with Medicaid law. Prior use of withholding has been limited. When CMS has used withholding as a compliance tool in the past, it withheld between 1 and 10 percent of the federal share of Medicaid spending. Prior withholdings appear to have been used when states incorrectly restricted eligibility or benefits, thus failing to comply with minimum requirements regarding access to coverage or eligibility. Minnesota’s case is different because of the scope of the proposed withholding and because the proposed withholding would be to address potential future fraud, rather than state policies that restrict Medicaid eligibility or benefits. The announced level of withholding represents nearly 20% of the federal share of Minnesota’s spending on an annual basis.

To withhold federal Medicaid funds, CMS must first provide states with the opportunity for an administrative hearing, and withholding generally ends when CMS is satisfied with states’ resolution of the issue. Withholdings may reflect issues with states’ Medicaid approved plans or with states’ implementation of the plans. Because CMS has authority to approve states’ plans, most issues arise regarding implementation of the plan and are resolved using a corrective action plan. Corrective action plans may also be used to address other types of program integrity issues in Medicaid (such as payment error rates or eligibility re-determinations). In general, the plans include a narrative of steps states are planning to take to address issues related to proper implementation of the Medicaid program. On January 13, 2026, Minnesota requested a hearing about the withholding and on January 30, 2026, Minnesota submitted a revised corrective action plan to CMS. If requested, CMS is required to schedule a hearing for Minnesota within 60 days of issuing notice (which would have been March 7, 2026) but CMS has not done so as of March 16, 2026. It is unclear whether that means CMS has accepted the state’s revised corrective action plan or what the next steps might be.

What are the implications of new reliance on deferrals and withholds?

The new approach to federal Medicaid spending when fraud is suspected creates uncertainty for state budgets, particularly given the magnitude of federal funding at stake and the time it takes to resolve administrative disputes. Unlike the federal government, states must generally operate balanced budgets, which is one reason states are able to draw down matching funds to finance ongoing expenditures. The immediate loss of federal funds via withholding could make it difficult for states to maintain current programs while details of the cases are being sorted out. More extensive use of deferrals could have similar destabilizing effects on states’ budgets because they reduce the amount of federal funds available to states for several months. Deferrals also place a new administrative burden on states to demonstrate the allowability of expenditures and may increase the likelihood of disallowances. Because disallowances often take years to resolve, increased rates of disallowances would further exacerbate states’ budget uncertainty. Other approaches to addressing suspected fraud, waste, and abuse remain available to CMS. The National Association of Medicaid Directors (NAMD) has suggested the following actions to help states to address fraud waste, and abuse in Medicaid:

- Help states identify federal materials about best practices such as recommendations and provider enrollment self-assessments;

- Create rapid methods to share information about provider disqualifications between Medicare, the Veterans’ Health Administration, and Medicaid;

- Respond more quickly to fraud reports from state attorneys general and the Medicaid Fraud Control Units;

- Strengthen procedural pathways for states and CMS to work collaboratively on Corrective Action Plans to enhance adherence to provider requirements while maintaining access to Medicaid benefits;

- Conducting additional analysis of Medicaid data through the Center for Program Integrity;

- Strengthening federal data sources and their interoperability; and

- Providing technical assistance to state officials and staff.

New uncertainty about the availability of federal funding could have implications for Medicaid enrollees and providers who are not involved in fraud. If states have inadequate funding to maintain existing Medicaid services, they may face difficult decisions regarding how to limit Medicaid spending. In general, states can reduce Medicaid spending by decreasing payment rates for providers, covering fewer services, or enrolling fewer people. Such actions could affect enrollees and providers who are not using or providing services in which fraud is suspected. There will also be additional disruptions for providers who lawfully provide Medicaid services where fraud is suspected because of new administrative burdens associated with increased audits, delayed payments, and other administrative practices.

CMS’ new approach to addressing cases of suspected fraud may exacerbate administrative and financial challenges states face as they implement the 2025 reconciliation law. The 2025 reconciliation law made historic reductions in federal funding for Medicaid and created new administrative requirements for states, particularly those that must implement work requirements for enrollees eligible for Medicaid through the Affordable Care Act Medicaid expansion. As states work to implement those changes and adjust to changes in federal financing, the new approach to fraud creates additional administrative requirements and potential new reductions in federal funding. Combined, these changes may have more significant implications for states’ ability to maintain existing levels of Medicaid payment rates, coverage, and eligibility.