About the Survey

At the end of 2025, despite a government shutdown over the policy, the enhanced premium tax credits expired, decreasing financial assistance for subsidized Marketplace enrollees and contributing to significant increases in the Affordable Care Act (ACA) Marketplace costs for most enrollees overall. Amid the debates leading up to the expiration, KFF conducted a probability-based survey of 1,350 adults covered by ACA Marketplace plans in late 2025 to better understand their worries about potential cost increases for their health coverage. Now—without the enhanced tax credits in place—KFF re-interviewed 1,117 individuals (more than 80% of the original sample) to learn how they are navigating these changes to the ACA Marketplace.

This report is based on all 2025 Marketplace enrollees who took the follow-up survey, including returning Marketplace enrollees1, those who have left the Marketplace entirely for another type of coverage, and those who are now uninsured.

Summary of Findings

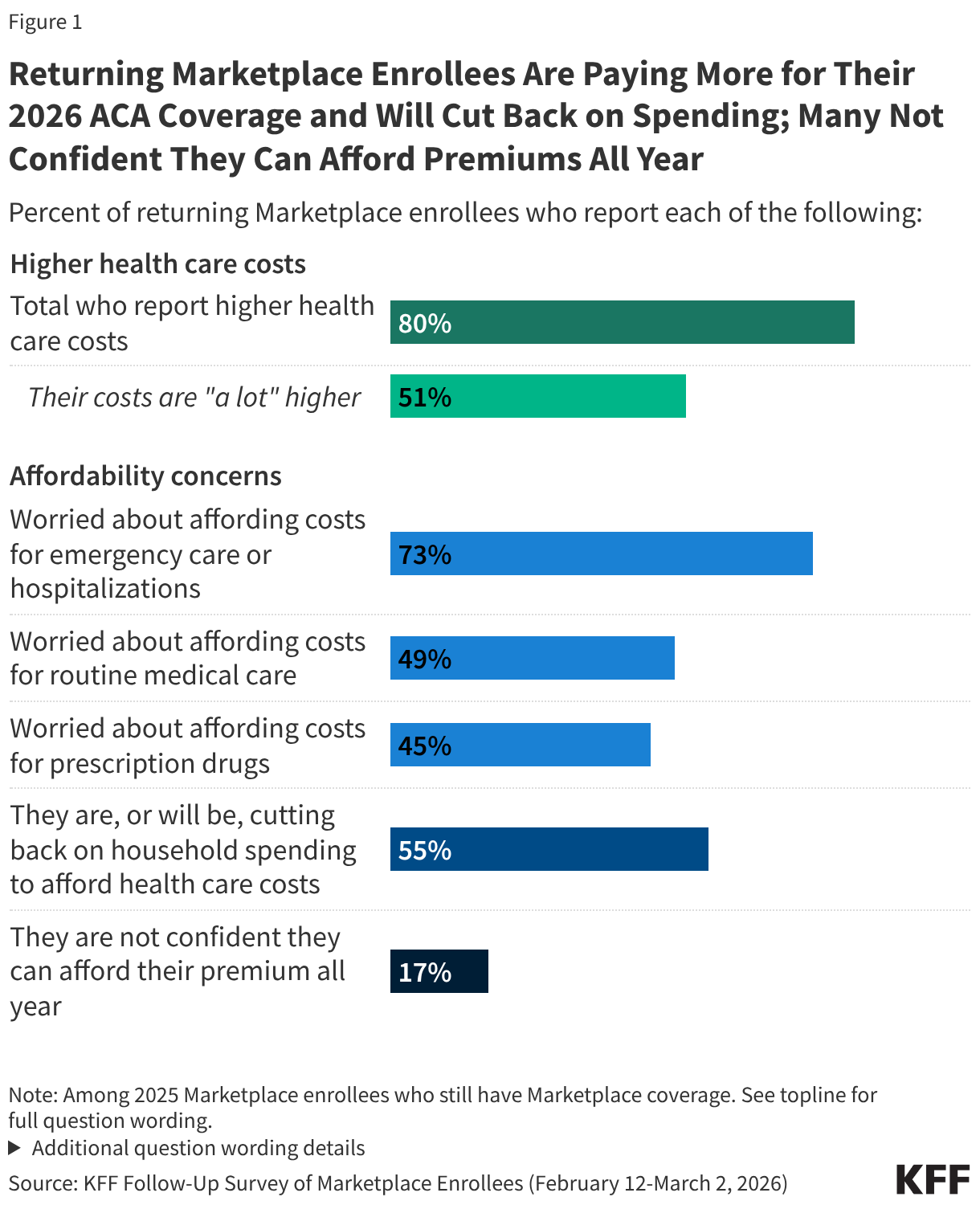

Half of those who have re-enrolled in ACA Marketplace coverage say their health care costs are “a lot higher” this year. Following the expiration of the enhanced premium tax credits and an open enrollment period that left many Affordable Care Act (ACA) Marketplace enrollees feeling “worried” and “angry,” most of those who have re-enrolled in Marketplace coverage now report paying more for coverage. A large majority (80%) of returning Marketplace enrollees say their 2026 plan’s premiums, deductibles, or coinsurance and co-pays are higher than last year, including half (51%) who say they are “a lot higher.”

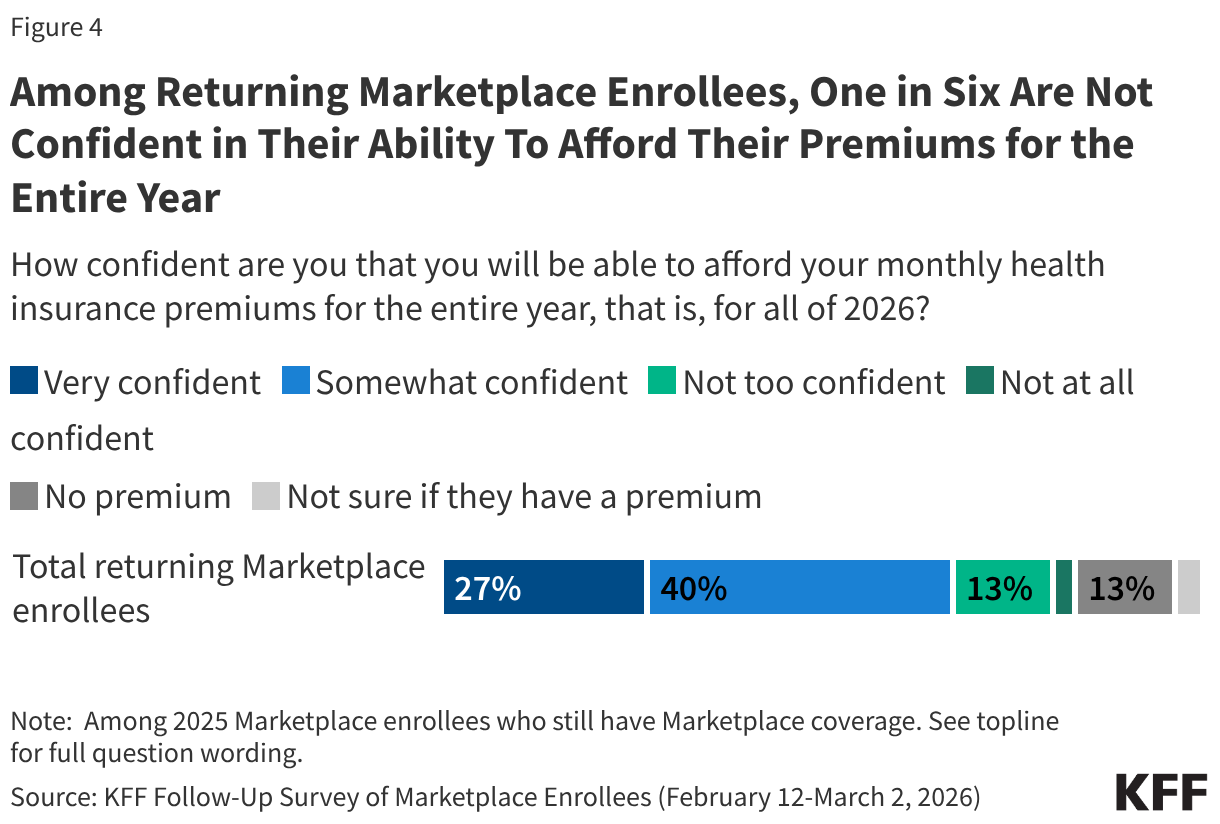

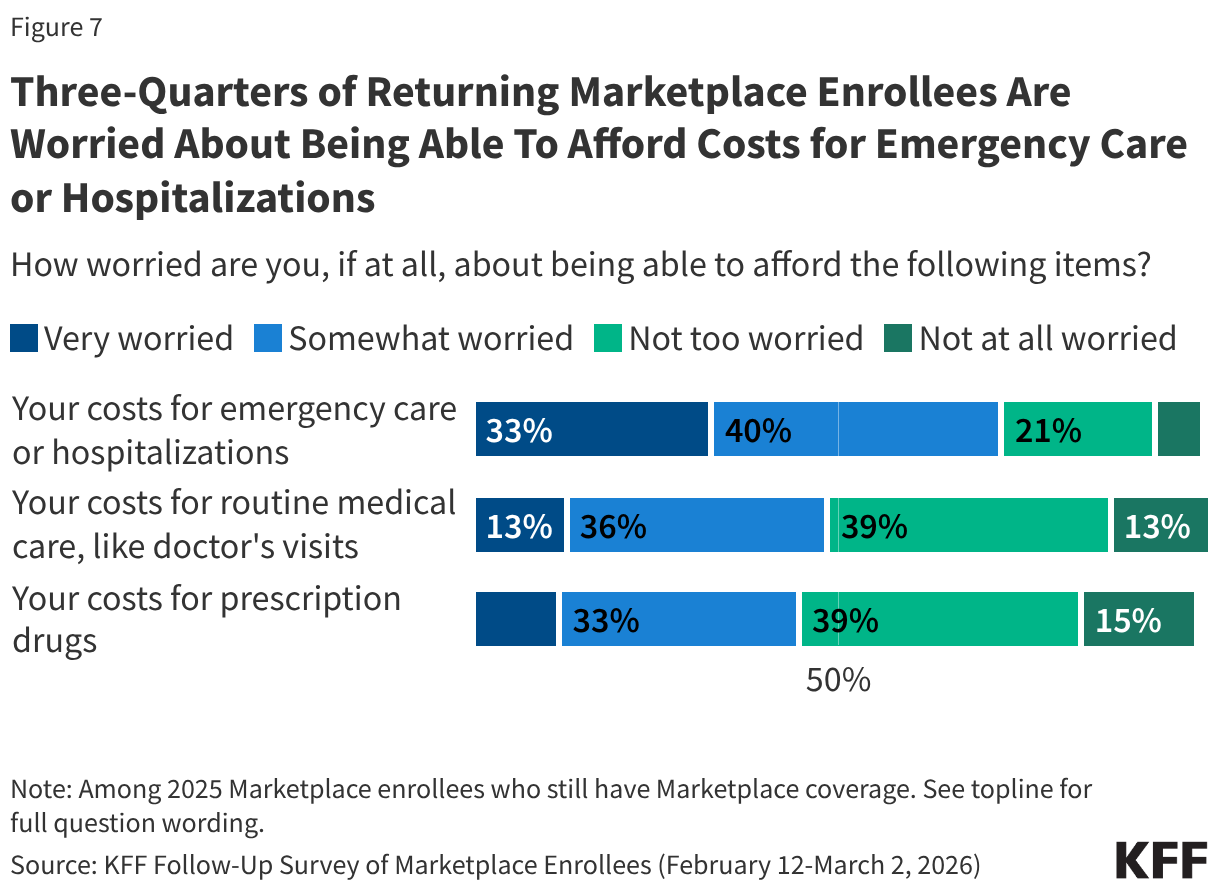

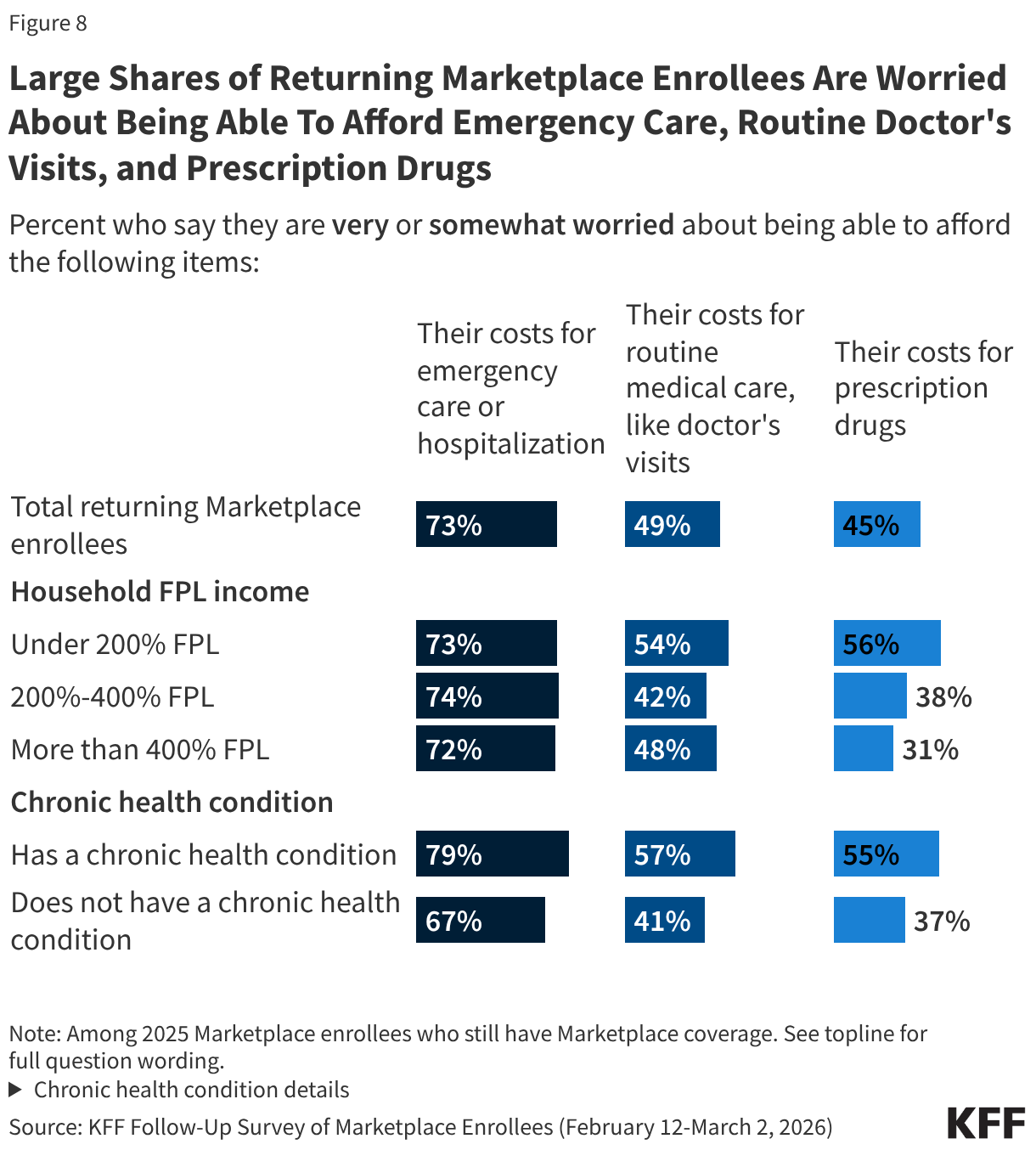

ACA Marketplace enrollees worry about affording their monthly premiums, as well as out-of-pocket expenses such as emergency care or routine medical visits. With many returning Marketplace enrollees reporting higher costs this year, majorities express worry about affording both routine and unexpected medical care. Three in four (73%) returning Marketplace enrollees say they are “very worried” or “somewhat worried” about being able to afford costs for emergency care or hospitalizations while about half are worried about affording costs for routine medical visits (49%) or prescription drugs (45%). Worries are even greater among those with lower incomes and those with chronic health conditions. In addition, one in six (17%) returning Marketplace enrollees say they are not confident they will be able to afford their monthly health insurance premium for the entirety of 2026. This is even as a quarter of those who switched plans say they downgraded their plan’s metal tier (e.g. from a Silver plan to a Bronze plan) in 2026, which generally have lower premiums but typically have higher out-of-pocket costs.

Health care costs are straining household budgets. Among 2025 Marketplace enrollees who have re-enrolled in Marketplace coverage, many report that their health care costs are putting pressure on household budgets. A majority (55%) of returning Marketplace enrollees say they are (or will be) cutting back spending on food or basic household items in order to afford the costs of coverage and care. The impact is even harder for returning enrollees with chronic health conditions, with 62% saying they are, or will be, cutting back on food and other household items in order to help them afford their health care costs.

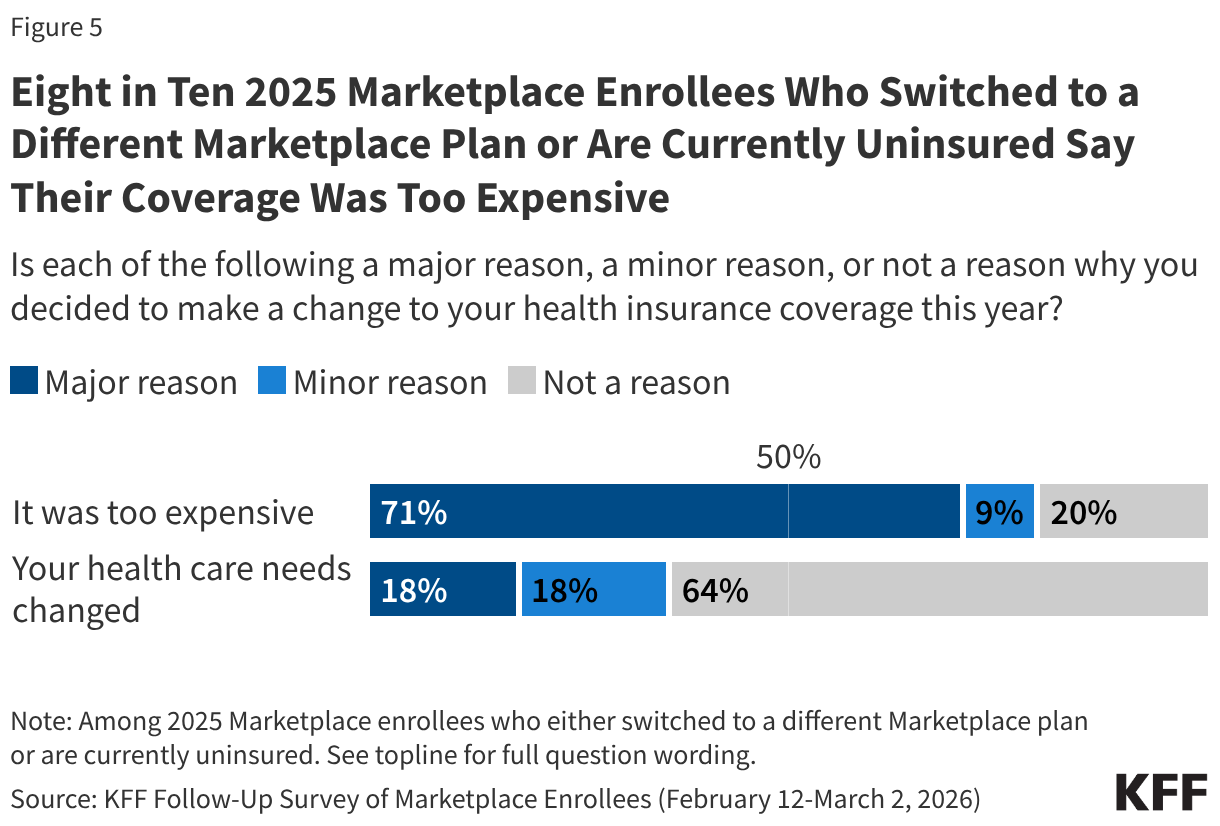

Some previous ACA Marketplace enrollees are now uninsured or have changed to a different Marketplace plan, citing costs as the major reason for that decision. One in ten (9%) 2025 Marketplace enrollees say they are now currently uninsured and three in ten (28%) say they switched to a different Marketplace plan. When asked the reasoning behind their change, a larger share say costs were the driver rather than changes to their health care needs. A 34-year-old man living in Texas put it this way, “The prices are simply too high. $800/month for the absolute cheapest plan for two people. Our income is $120k, so we don’t qualify for subsidies in Texas. I don’t think we could afford our mortgage if I had to pay for health insurance.”

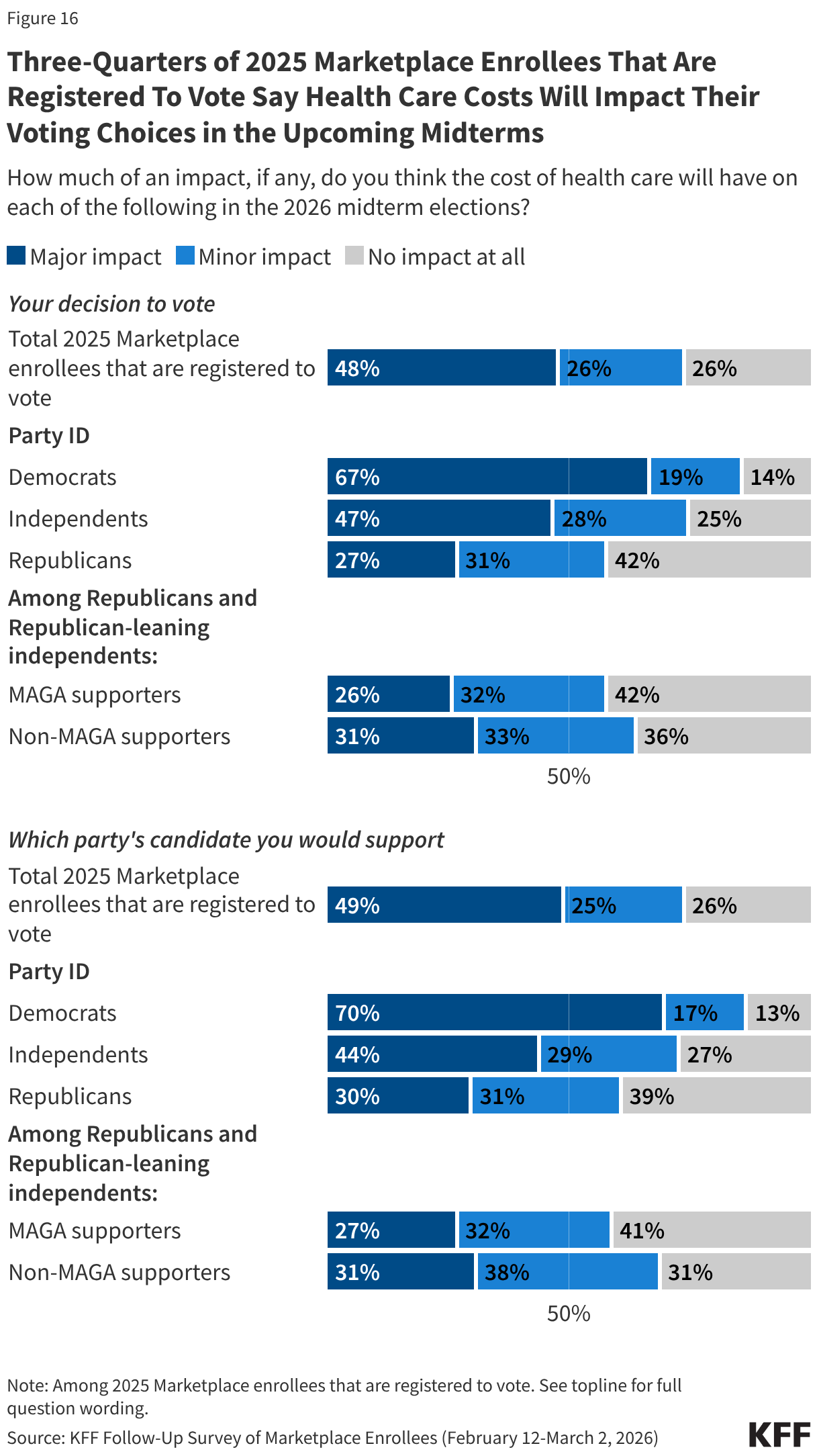

Health care costs may be a deciding factor for ACA Marketplace enrollees in the 2026 midterm elections. With health care costs front and center for 2025 Marketplace enrollees, many who are registered to vote say that the cost of health care will have a major impact on their decision to vote (48%) and which party’s candidate they will support (49%) in the midterm elections. The issue currently resonates more with Democrats, who are more than twice as likely as Republicans to say health costs will play a major impact on their decision to vote in the 2026 midterms (67% vs. 27%) and on which candidate they decide to vote for (70% vs. 30%).

Where Are They Now? Coverage Changes Among 2025 Marketplace Enrollees

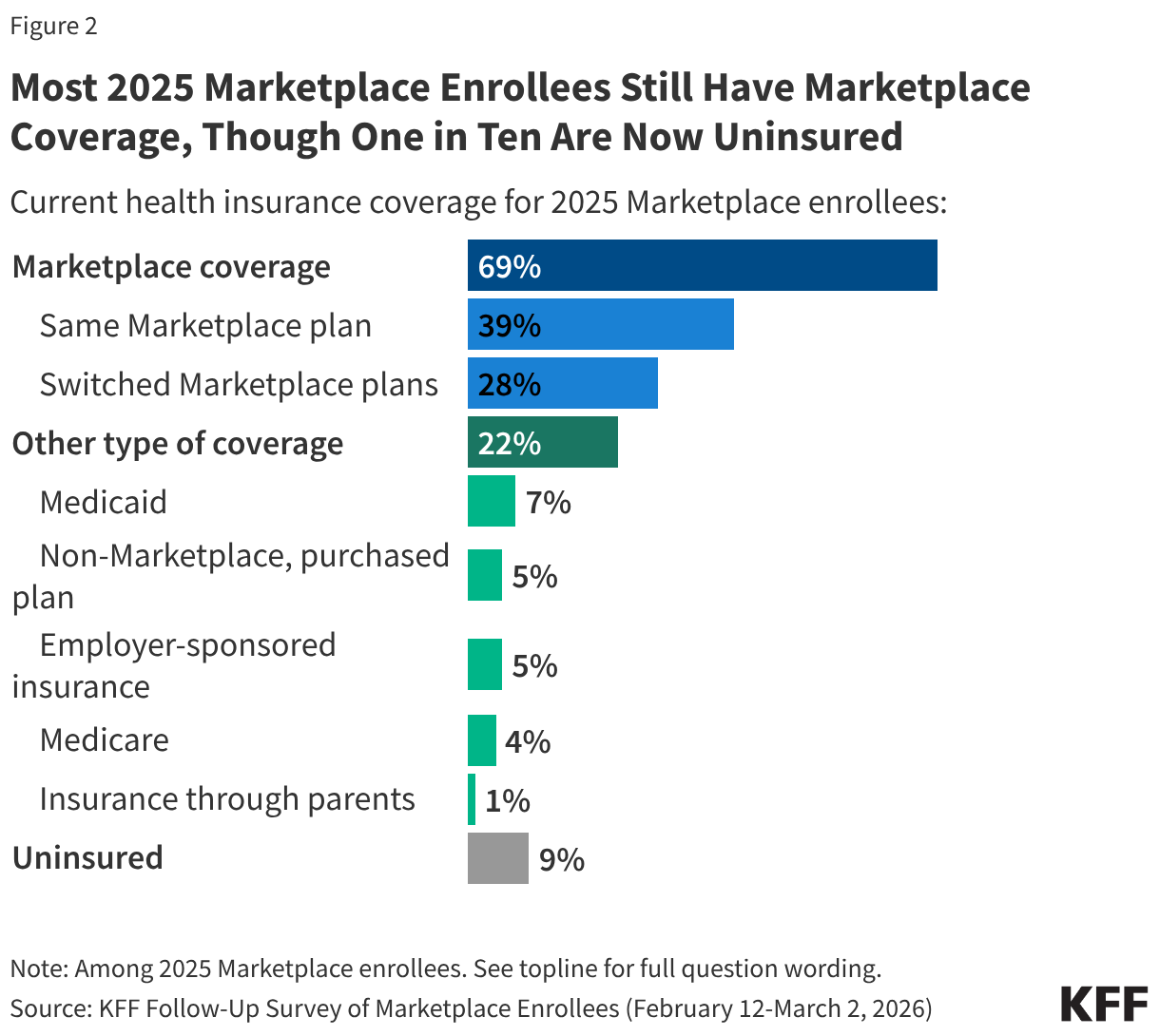

The Follow-Up Survey of ACA Marketplace Enrollees finds most (69%) 2025 enrollees say they have re-enrolled in Marketplace coverage for 2026, including four in ten (39%) who say they are enrolled in the same plan they had in 2025 and nearly three in ten (28%) who have switched to a different Marketplace plan. This is largely consistent with the 2025 survey findings in which a third said they would be “very likely” to look for a different Marketplace plan if their premiums doubled.

Additionally, about three in ten 2025 Marketplace enrollees now say they no longer have Marketplace coverage, including 22% who transitioned to a different source of coverage, such as through an employer, by becoming eligible for programs like Medicare or Medicaid, or say they have now purchased a non-Marketplace health insurance plan (some of which may provide less comprehensive coverage and have fewer consumer protections than Marketplace plans). One in ten (9%) 2025 Marketplace enrollees say they are currently uninsured. A large amount of churn on and off the Marketplace is normal as ACA Marketplace coverage is often a temporary source of coverage between jobs, and because income, age, and other circumstantial changes can make people newly eligible for other public programs such as Medicaid or Medicare.

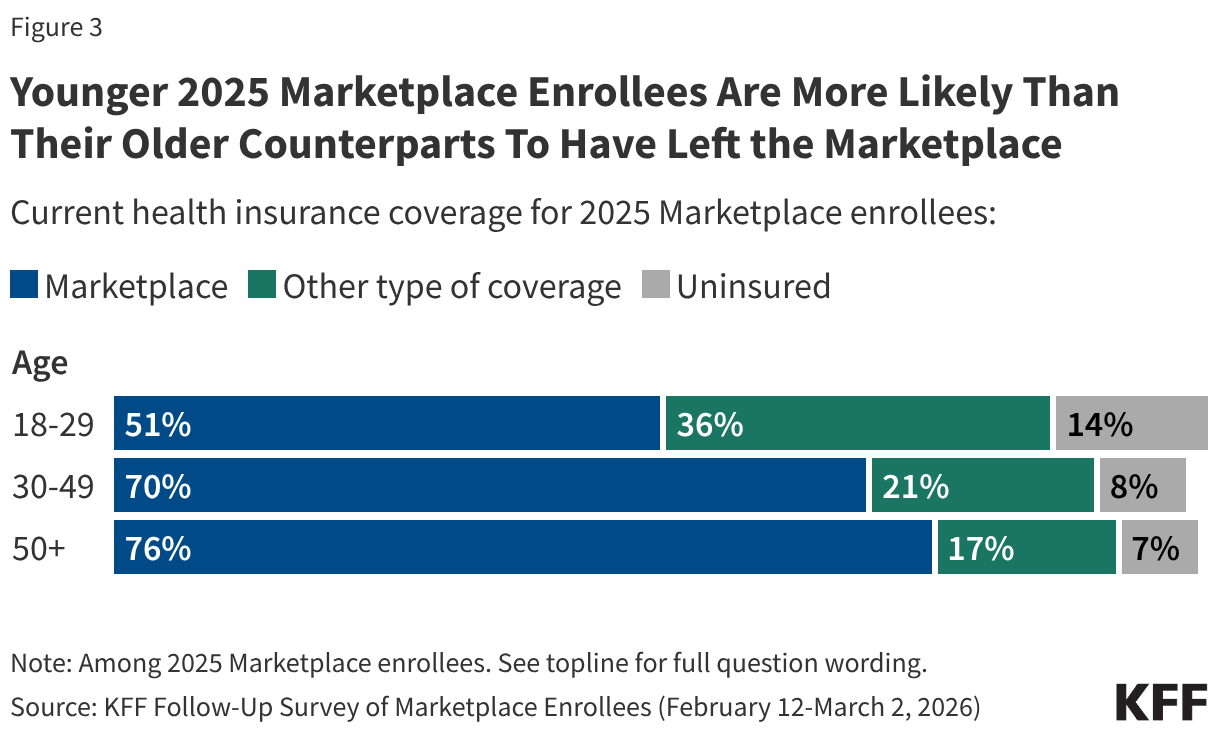

Notably, half (49%) of younger 2025 Marketplace enrollees between the ages of 18 and 29 report having left the Marketplace entirely, including 14% who say they are currently uninsured. In contrast, smaller shares of older 2025 Marketplace enrollees—ages 50 and up—say they are currently uninsured (7%). Additionally, younger 2025 enrollees are also more likely than their older counterparts to say they have left the Marketplace for another source of coverage—which would be expected with life changes such as starting a new job, getting married, or experiencing a change in income. Significant shares of younger adults having left the Marketplace in 2026 is consistent with previous KFF policy analysis on the expiration of the enhanced tax credits, which attributes part of this year’s increases to insurers anticipating healthier (e.g. younger) adults exiting the Marketplace, creating an enrollee base that is more expensive on average.

Among those who still have a Marketplace plan, one in six (17%) returning enrollees say they are “not too” or “not at all” confident they will be able to afford their insurance premiums for all of 2026. This may put them at risk of losing their Marketplace coverage at some point this year.

Additionally, 4% of returning Marketplace enrollees say they have yet to pay their first premium for 2026. Notably, returning enrollees who receive tax credits to help pay for their coverage are generally provided with a 3-month grace period for nonpayment of premiums, meaning most may have until the end of March to pay any premiums that are due before facing the retroactive termination of their health insurance coverage.

Costs Are a Major Reason Why Enrollees Switched to a Different Marketplace Plan or Dropped Coverage

Almost four in ten (37%) 2025 enrollees are either uninsured or switched to a different Marketplace plan. When asked the reasoning behind their change, a larger share say costs were the driver rather than changes to their health care needs. Eight in ten say they made a change to their coverage because it was too expensive, including seven in ten (71%) who say this was a “major reason” and one in ten (9%) who said it was a “minor reason.” Just over a third (36%) say changing health needs were a major or minor reason why they changed plans or dropped their Marketplace coverage.

Many 2025 enrollees who switched Marketplace plans this year say their previous plans’ premiums increased dramatically when selecting coverage for 2026. Additional reasons for changing plans include their old plans no longer being available and general dissatisfaction with their previous plan.

In Their Own Words: What is the main reason you switched to a different Marketplace plan this year?

“The cost of the same plan I had in 2025 tripled in price to $360/month. So I went with a different plan that cost less. But even it was higher than the plan I had in 2025.” – 62-year-old man, Wisconsin

“The price went from 2k to 3500 for a household of 4 people.” – 37-year-old man, Florida

“Income exceeded the subsidy limit, forcing us to pay the full cost, so we switched down to a bronze from a gold plan. Even doing that our premiums are 3 times what they were in 2025, with lower plan features and a higher deductible.” – 56-year-old man, Texas

“Cost. By switching to Bronze, I would receive a tax credit that covered my plan. If I had stayed on my Silver plan, I would’ve had to pay out-of-pocket, which my budget does not allow for.” – 26-year-old woman, Montana

“In 2025 I had the elite bronze plan. The monthly premium cost of the plan I had in 2025 went up, the PCP and prescription copays went up, and the deductible went up almost $4000. To keep my out of pocket expenses the same and given my prior history…I had to drop to the everyday bronze with a much larger deductible and just hope that I continue not to actually need anything unexpected.” – 55-year-old man, South Carolina

Health Care Costs Weigh Heavily on the Now Uninsured

Among the 9% of 2025 enrollees who say they are currently uninsured, survey responses indicate that the cost of health care played a major role in their decision to drop coverage, and many from this group report worrying about affording medical care.

In Their Own Words: What is the main reason you are currently without health insurance coverage?

“The end of ACA subsidies caused a huge increase in premiums, the cost of which I could not afford.” – 63-year-old man, California

“Even though I make some income (too much for subsidies, even last year), the increase is so high even for those without subsidies. I simply cannot afford to pay $1,200 a month for insurance. It used to be high premiums meant low deductibles and copays, but not anymore. This is ridiculous. $1,200 for a healthy person, and an $8,000 deductible. Really?” – 56-year-old woman, Illinois

“[I am] self-employed and [there are] no cheap health plans.”– 24-year-old man, Florida

“Without the subsidy, I cannot afford the premium payments.”– 54-year-old man, Texas

“The prices are simply too high. $800/month for the absolute cheapest plan for two people. Our income is $120k, so we don’t qualify for subsidies in Texas. I don’t think we could afford our mortgage if I had to pay for health insurance. $800/month is 8 self pay doctors visits a month. If I have a catastrophic health event it makes more sense for me to just declare bankruptcy than it would be to be delinquent on other payments.” – 34-year-old man, Texas

Many 2025 enrollees who are now uninsured cite fears about accessing and affording care in the case of unexpected medical emergencies. Some who have significant health issues say their main worry about not having health insurance is being unable to afford necessary medications and treatment.

In Their Own Words: What is your main worry, if any, about not currently having health insurance?

“Not managing ongoing health issues and pre-existing conditions.” – 48-year-old woman, Colorado

“Everything. Can’t afford insurance can’t afford health care without insurance so basically just hoping and praying I don’t get sick or have any major issues pop up.” – 38-year-old man, Alabama

“We are 59 and 61 yrs old. We need healthcare. And now we will either avoid seeing a dror go bankrupt.” – 59-year-old woman, Virginia

“I’m in my ‘50s and have some health concerns that I won’t be able to address this year.” – 55-year-old man, Idaho

Health Care Costs Contribute to Affordability Worries and Challenges Among Returning Marketplace Enrollees

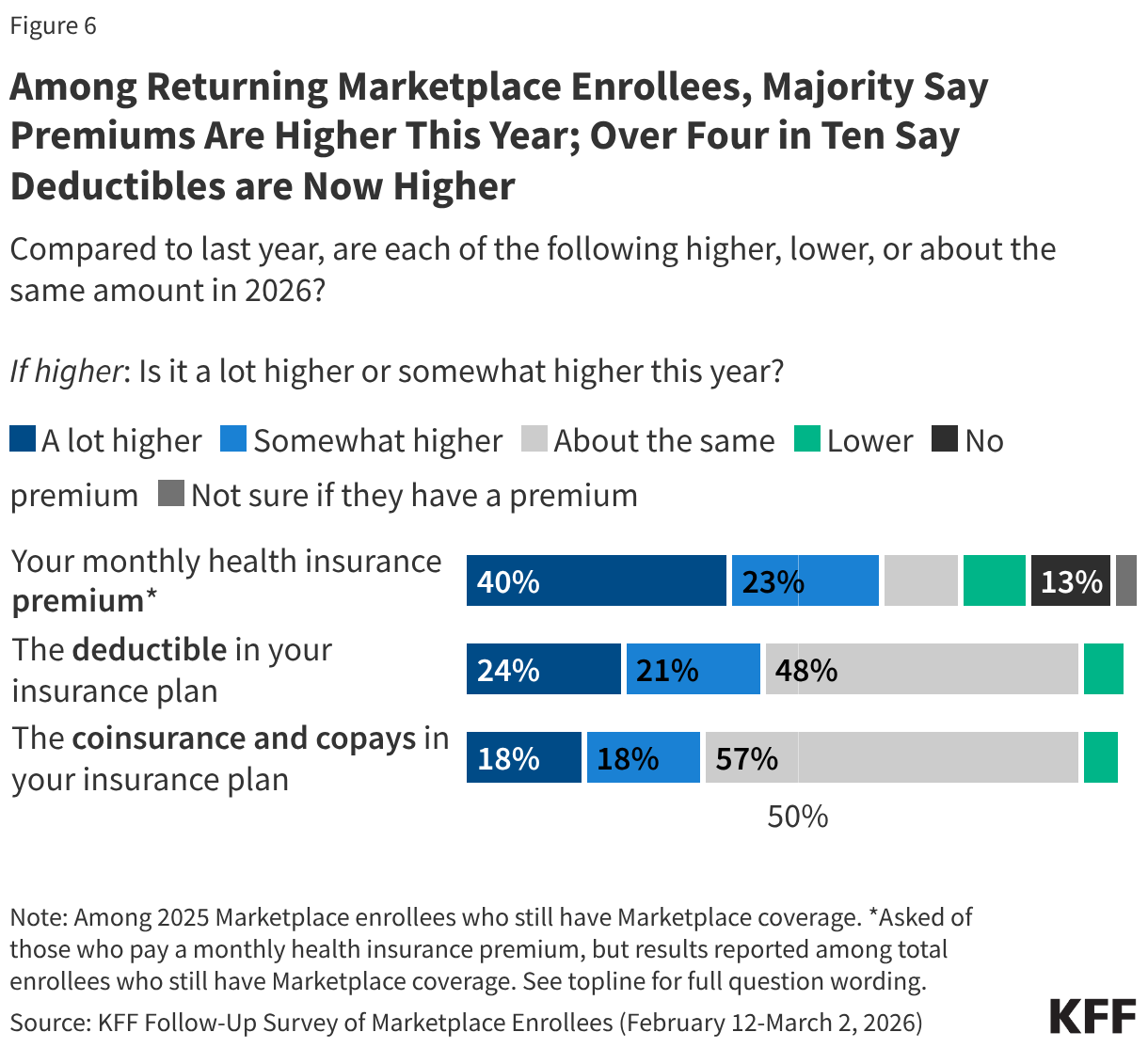

Following the expiration of the ACA enhanced premium tax credits in December 2025, a large majority (80%) of returning Marketplace enrollees say their health care costs are higher this year compared to 2025. This includes half (51%) of returning enrollees who say their health care costs—whether it be their premiums, deductibles, and/or their coinsurance and co-pays—are “a lot higher” compared to last year.

About six in ten (63%) returning Marketplace enrollees say their monthly health insurance premium is higher than 2025, including 40% who say it is “a lot higher.” In addition, nearly half say their deductibles are higher (45%, including 24% who say they’re “a lot higher”), and one-third say their coinsurance and co-pays are higher compared to last year (36%, including 18% “a lot higher”).

Increases in insurance plan cost-sharing are pronounced among those who say they switched their Marketplace plan this year. Over half (54%) of returning enrollees who switched plans say their deductibles are higher this year compared to last year (including 34% who say “a lot higher”), and an additional four in ten (42%) say their coinsurance and co-pays are higher (25% “a lot higher”). This likely reflects the fact that some enrollees switched to lower tier Bronze plans which may mitigate some of the increase in premiums but typically have higher out-of-pocket costs. Overall, a quarter (26%) of plan switchers say they downgraded their metal plan (e.g. from a Silver plan to a Bronze plan) in 2026.

While most 2025 Marketplace enrollees say they still have Marketplace coverage in 2026, having insurance does not insulate them from worrying about the costs of accessing care. About three in four (73%) returning Marketplace enrollees say they are “very worried” or “somewhat worried” about being able to afford costs for emergency care or hospitalizations while about half are worried about affording costs for routine medical visits (49%) or prescription drugs (45%).

At least seven in ten returning Marketplace enrollees across income groups say they are worried about being able to afford costs for emergency care or hospitalization. However, those with lower incomes are more likely than their higher-income counterparts to worry about being able to afford prescription drugs. Those with chronic conditions are more likely than those without such conditions to worry about affording emergency care, routine care, and the cost of prescription medications.

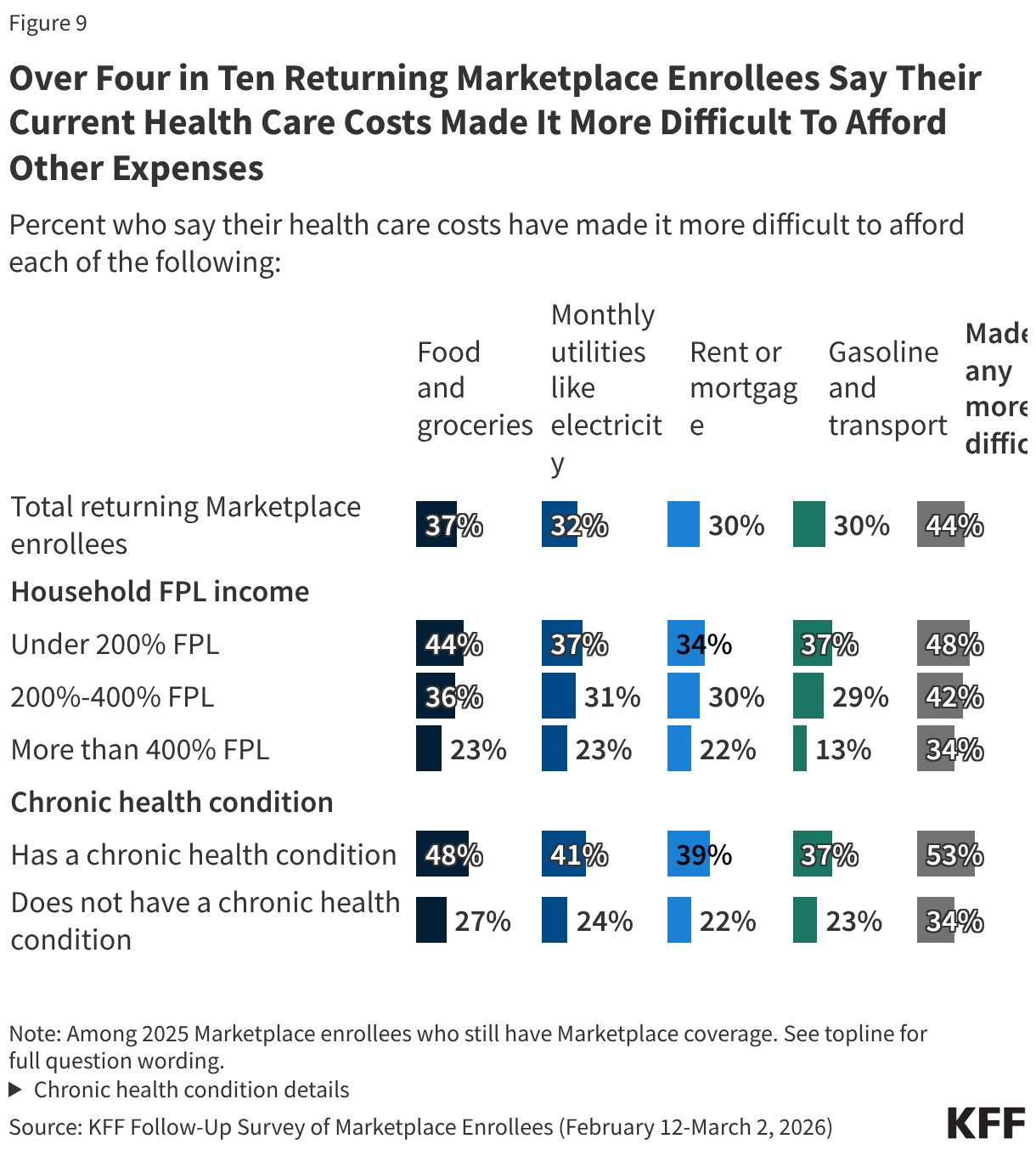

Rising health care costs can place considerable pressure on household budgets and create additional financial strain. Just over four in ten (44%) returning Marketplace enrollees say their health care costs have made it harder to afford other expenses, including over a third (37%) who say it has made it more difficult to afford food and groceries and about three in ten who say it has made it more difficult for them to afford their monthly utilities (32%), their rent or mortgage (30%), or gasoline or other transportation costs (30%)

About half of returning Marketplace enrollees with lower household incomes and those with chronic health conditions report that their health care costs are placing financial strain on other expenses.

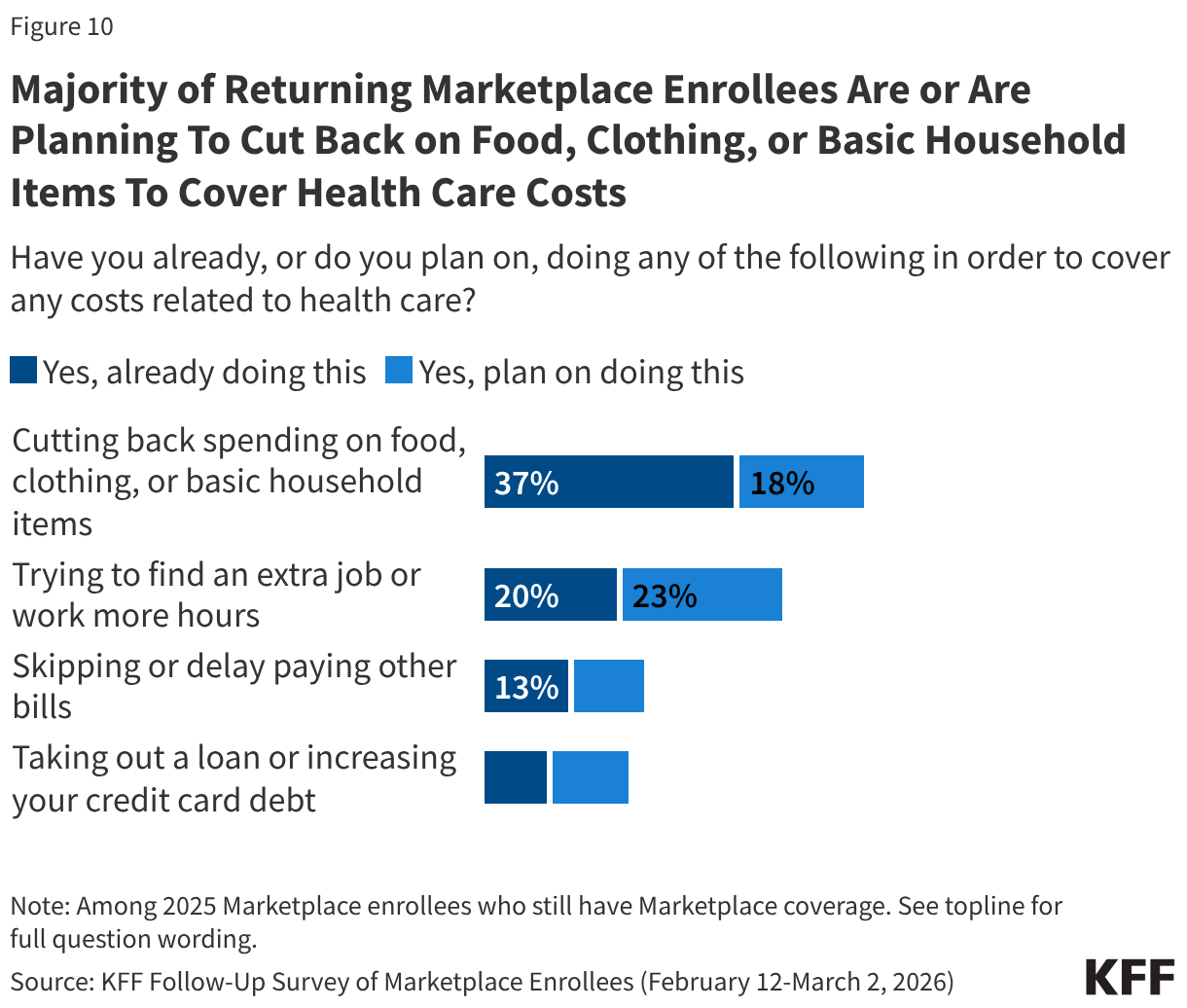

A majority (55%) of returning Marketplace enrollees say they have already, or are planning to, cut back spending on food or basic household items in order to cover any health care related costs. Around four in ten (43%) say they have already or are planning to find an extra job or work more hours to cover health expenses, while about two in ten are skipping or delaying paying other bills (23%) or taking out loans or increasing their credit card debt (20%). Notably, while one in five returning enrollees say they are already looking for another job or trying to find more hours, an increase in income could help them afford their premium or deductible payments, but it could also mean they become eligible for less financial assistance.

Returning Marketplace enrollees with chronic conditions are among the most likely to report taking steps to cover their costs, with about six in ten (62%) saying they have or plan to cut back on spending, half (52%) saying they have or plan to work more, a third (33%) saying they will skip or delay paying bills, and a quarter (26%) saying they will take out a loan or increase their credit card debt.

In Their Own Words: What changes or actions have you taken or think you may take in order to afford your health care costs this year?

“Attempt to pay off loans to free up more monthly money, budget groceries more tightly, put hospital debt on a payment plan.” – 24-year-old woman, Kentucky

“Cut back on food expenses, choose cheaper & fewer dining out experience, watch heat & AC usage even more.” – 54-year-old woman, California

“Attempt to use as little health care as possible. Make sure our doctors and hospitals are covered by the insurance. Talk with our doctors to verify that ordered treatments and/or drugs are really necessary. Discuss with providers/pharmacies to see if self-pay may be cheaper than using insurance in particular cases.” – 56-year-old man, Texas

“Shopping for cheaper groceries, not buying clothes, avoiding getting sick, not being as social.” – 63-year-old woman, California

“Pare back expenses as much as possible.” – 39-year-old man, Iowa

“Limit going to the doctor. I can’t afford the medications prescribed so I try to find over the counter substitutions.” – 54-year-old woman, Texas

“My grocery budget and fun budget are smaller so we can afford the premium.” – 38-year-old woman, Colorado

“I may have to get part-time employment. I may have to get a job after being retired.” – 60-year-old woman, Florida

Open Enrollment Process Left Many Marketplace Enrollees Worried and Angry

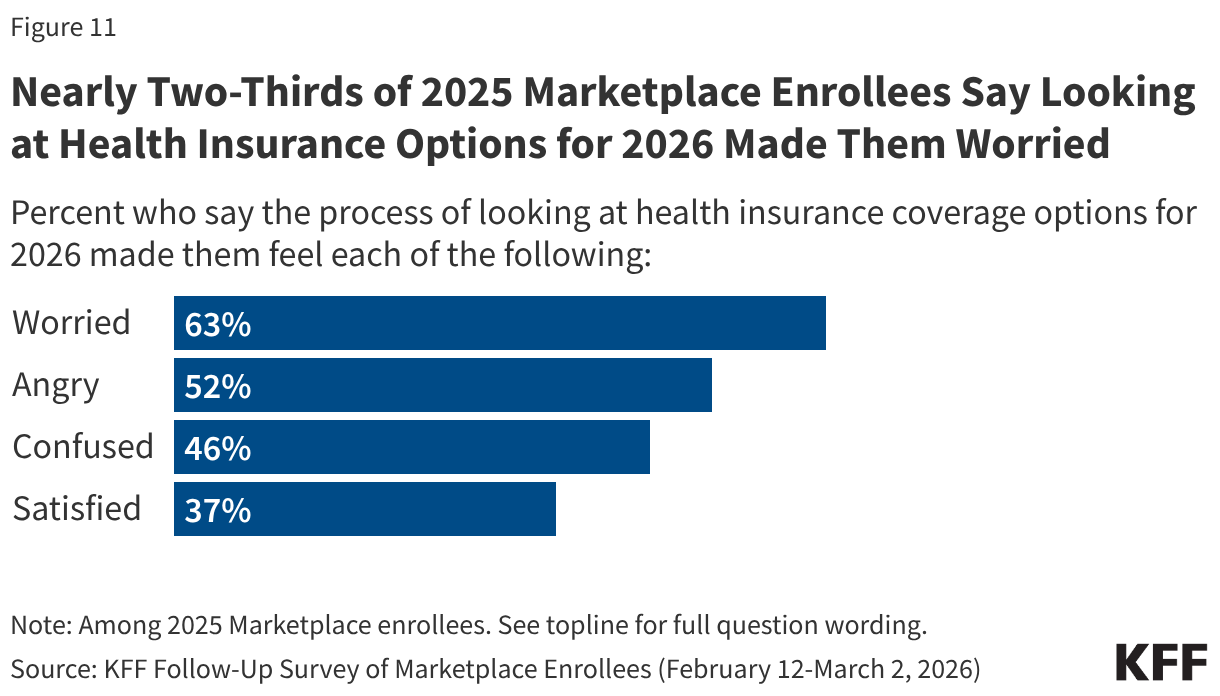

Following the expiration of the enhanced premium tax credits for ACA Marketplace coverage, many 2025 Marketplace enrollees say they felt worried or angry as they went through the process of evaluating their health insurance options for 2026. Nearly two-thirds (63%) of 2025 Marketplace enrollees say they felt “worried” during the process of looking for coverage while about half (52%) say they felt “angry.” Nearly half (46%) say the process made them feel “confused,” while nearly four in ten (37%) say they were “satisfied” during the process of looking for insurance coverage for this year.

Reactions to the Expiration of Enhanced Premium Tax Credits

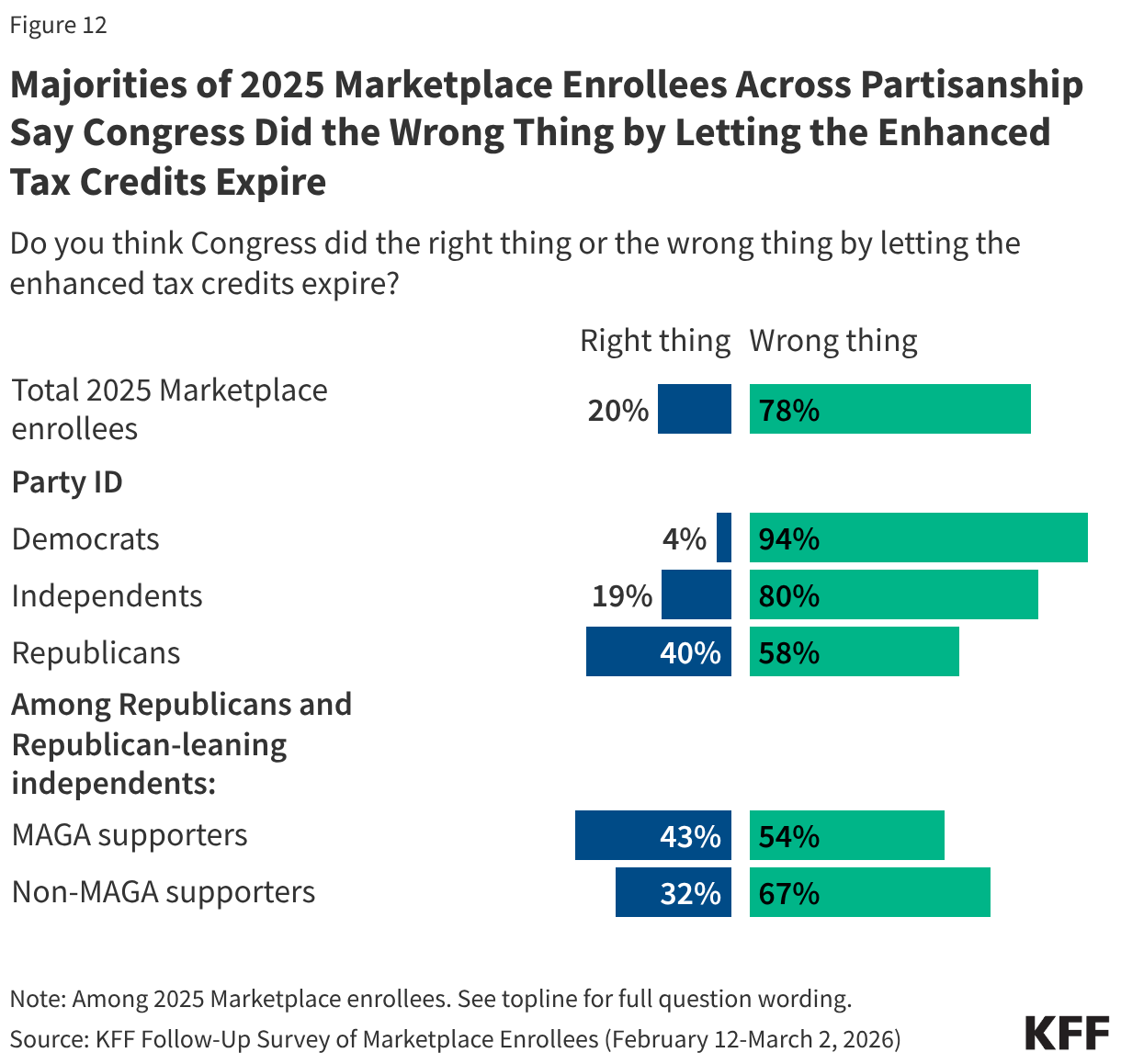

In a recent KFF Health Tracking poll, a majority of the public overall said Congress did the wrong thing by letting the enhanced premium tax credits for people who buy their insurance on the ACA Marketplace expire. Unsurprisingly, 2025 Marketplace enrollees share this sentiment, with eight in ten (78%) saying that Congress did the wrong thing by letting the credits expire, while two in ten say Congress did the right thing.

Majorities of 2025 Marketplace enrollees across partisanship agree that Congress did the wrong thing, including nearly all Democrats (94%), eight in ten independents, and six in ten Republicans (58%). Even among Trump’s base—Republicans and Republican-leaning independents who support the MAGA (Make America Great Again) movement—a majority (54%) say that Congress did the wrong thing by letting the credits expire.

When asked how they feel about the expiration of the enhanced premium tax credits, many 2025 Marketplace enrollees express anger, frustration, and disappointment. While some are fine with the expiration or note that it has not impacted them, many are upset at the rise in their own insurance costs and the government’s failure to extend the credits.

In Their Own Words: How do you feel about Congress letting the enhanced premium tax credits for the Affordable Care Act (ACA) expire?

“Angry. They get affordable good coverage even when they aren’t doing ANYTHING. We struggle to pay for health insurance. And they gut the ACA without offering any alternative.” – 60-year-old independent woman, California

“I am okay with it. It was not going to be able to sustain itself so it needed to happen.” – 48-year-old Republican woman, Florida

“Evil on the part of republicans. Absolutely ineffectual on the part of democrats.” – 33-year-old Democratic man, Washington

“It’s a disgrace that families are being put in this position to chose between health insurance and all other household needs.” – 42-year-old Democratic woman, Pennsylvania

“It could hurt some people but the impact to me is minimal.” – 56-year-old independent man, California

“There should have been a gradual decrease versus a sudden cut off or more communication so that people could prepare as needed and advocate where possible.” – 44-year-old Democratic woman, California

“I feel as if it’s unfair to those who make too much to be able to receive Medicaid. We are getting penalized for making more money than poverty level.” – 26-year-old independent woman, Florida

“It needs to expire and pharmaceutical companies need to have a cap on prices. They should not be able to charge so much. Also, put a cap on insurance company premiums too.” – 47-year-old independent woman, Georgia

“It has had a major financial impact on my already financially stressed household as I am fully disabled in a wheelchair and unable to work and also unable to receive disability or social security.” – 58-year-old Republican woman, Texas

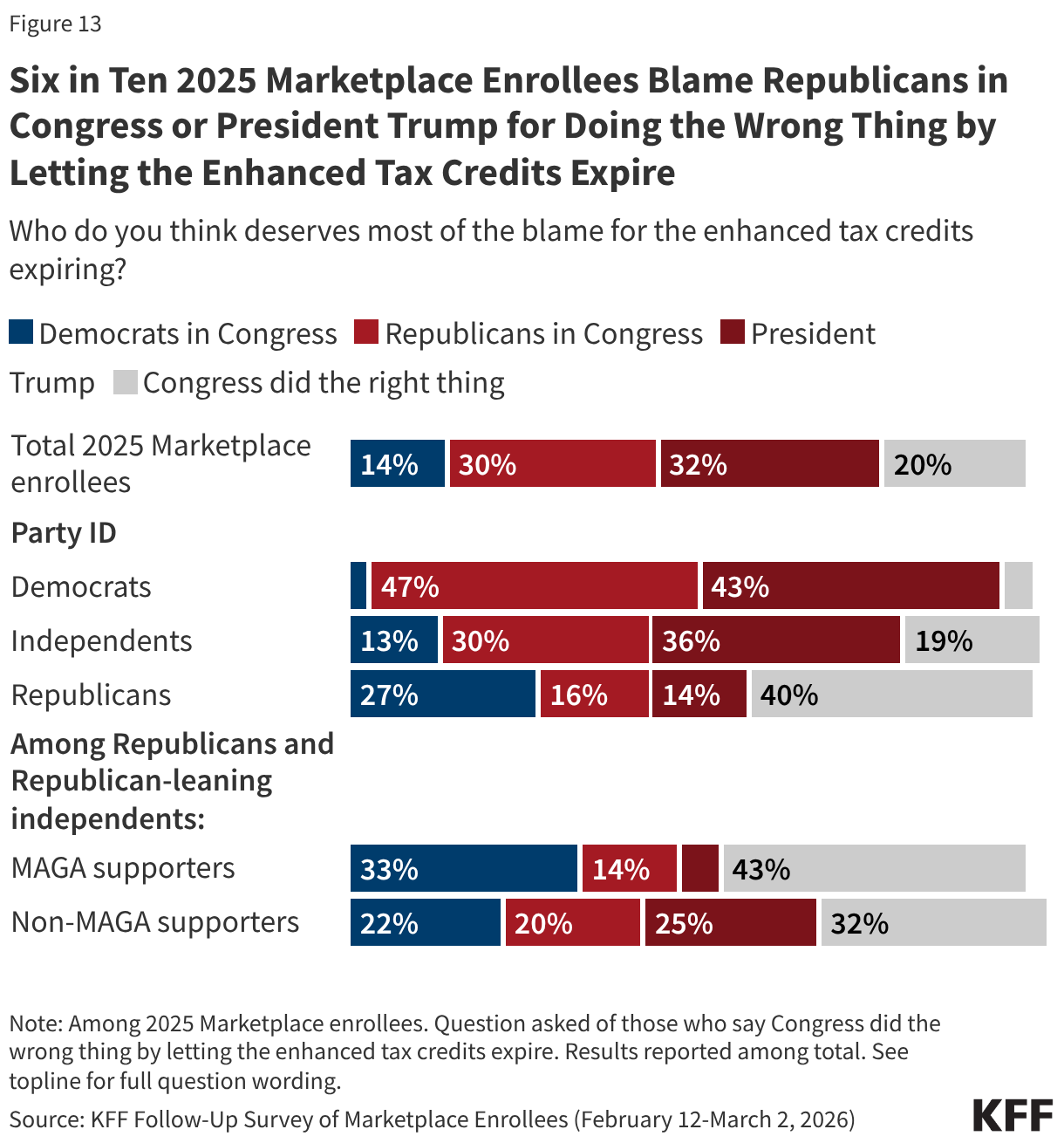

Among all 2025 Marketplace enrollees, about six in ten (62%) place the most blame on either President Trump (32%) or Republicans in Congress (30%), while a smaller share (14%) say Congressional Democrats deserve the most blame. Two in ten think Congress did the right thing by letting the tax credits expire.

While very few Democratic 2025 Marketplace enrollees blame their own party (3%) for the expiration of the enhanced tax credits, three in ten Republicans, including two in ten MAGA-supporting Republicans, place the most blame on either President Trump or Republicans in Congress.

Potential Political Impacts of Higher Health Care Costs Among Marketplace Enrollees

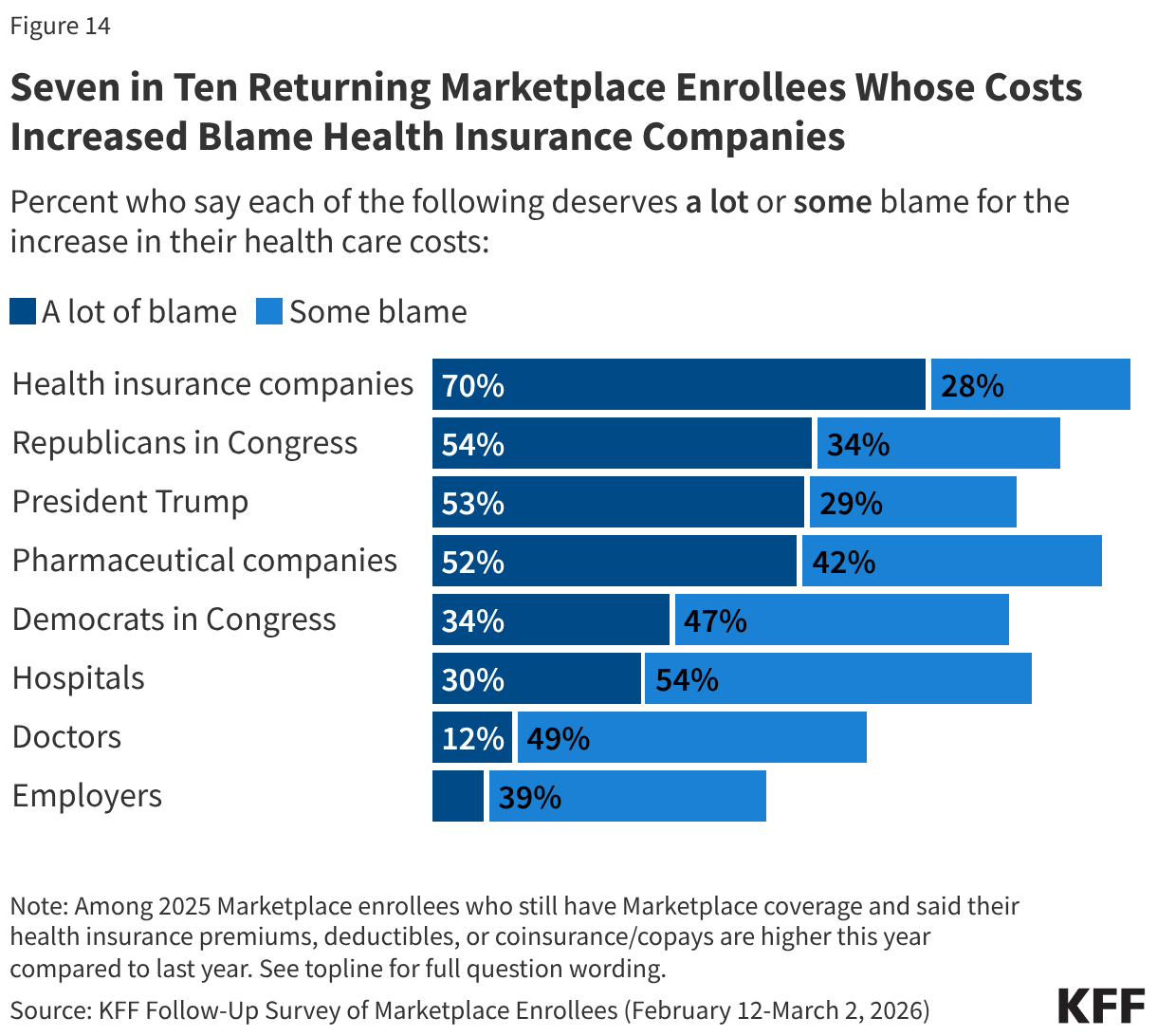

When it comes to increases in their own health care costs, returning Marketplace enrollees blame lawmakers alongside health insurance and pharmaceutical companies.

Among the eight in ten returning Marketplace enrollees who say their premiums or cost-sharing are higher this year, seven in ten say health insurance companies deserve “a lot” of blame for the increase. Although the public perceive health insurance companies as a major source of blame for their cost increases, lack of action by Congress in extending the tax credits is attributed as the main cause of increases in premiums and other costs according to KFF policy analysis. Majorities of returning Marketplace enrollees also say Republicans in Congress (54%), President Trump (53%), and pharmaceutical companies (52%) deserve “a lot” of blame for the increase in their health care costs. A third (34%) of returning Marketplace enrollees who report having higher health care costs say Democrats in Congress deserve “a lot” of blame. Fewer place “a lot” of blame on hospitals (30%), doctors (12%), or employers (8%). Notably, around half or more of those who report that their premiums, deductibles, or coinsurance and co-pays are higher this year than last year place at least some blame on each of the groups asked about.

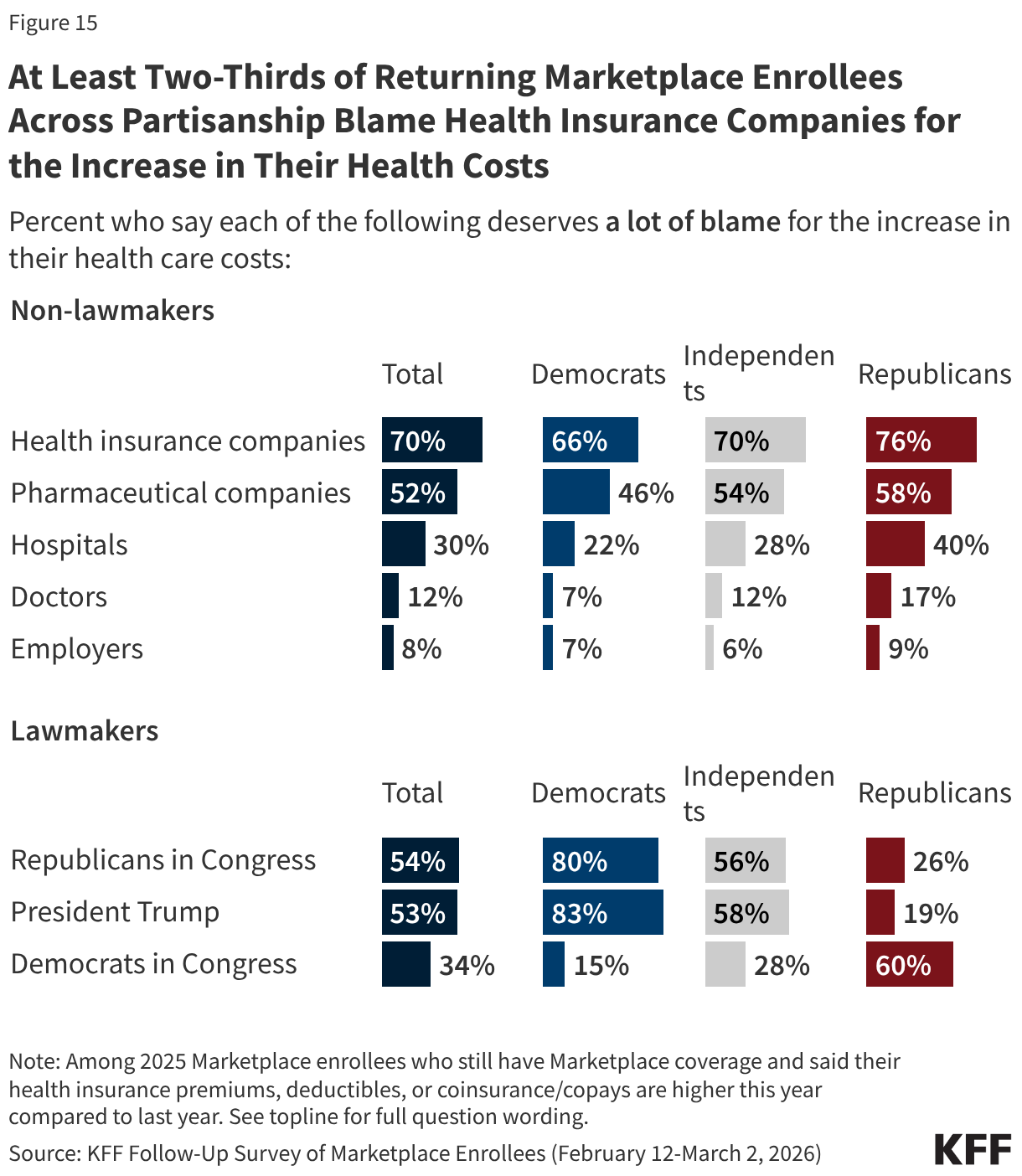

Across partisanship, at least two-thirds of returning Marketplace enrollees whose health care costs (including premiums, deductibles, or coinsurance and co-pays) are higher now than last year say health insurance companies deserve “a lot” of blame, and around half or more place “a lot” of blame for their increased costs on pharmaceutical companies. However, when it comes to lawmakers, there is a predictable partisan division. Among returning Marketplace enrollees with higher health care costs than last year eight in ten or more Democratic enrollees place “a lot” of blame on President Trump (83%) and on Congressional Republicans (80%) for their increased costs. In contrast, six in ten returning Republican enrollees who now have higher health care costs place “a lot” of blame on Democrats in Congress, as do MAGA supporting Republican enrollees.

Health care costs may impact enrollees’ decisions at the ballot box this November, and in some congressional districts, the number of Marketplace enrollees could be enough to swing close elections. Three-quarters of 2025 Marketplace enrollees who are registered to vote say the cost of health care will have a “major impact” or “minor impact” on their decision to vote (73%) and which party’s candidate they will support (74%) in the midterm elections. Majorities of voters across partisanship say health care costs will impact their voting decisions, however Democrats are more than twice as likely as Republicans to say it will have a major impact on their decision of whether to vote (67% vs. 27%) and on which party’s candidate they will support (70% vs. 30%). At least four in ten independent voters say that health care costs will have a major impact on their decision to vote (47%) and who they decide to vote for (44%).

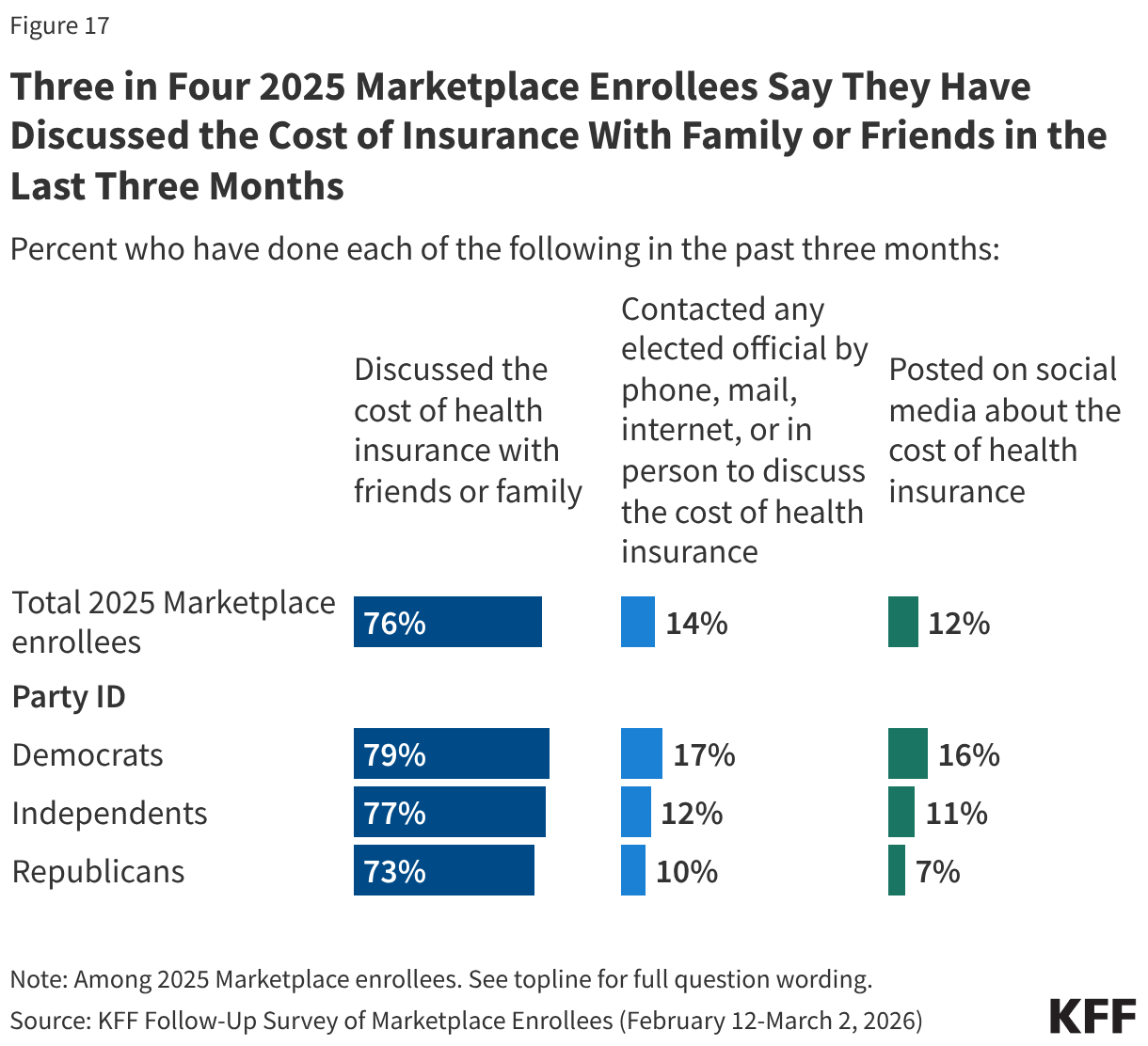

Beyond being motivated to vote, some enrollees have taken actions to discuss their rising health care costs with friends and family, online, or by directly contacting an elected official. Three-quarters (76%) of 2025 Marketplace enrollees have discussed the cost of health insurance with friends or family, including similar shares across partisanship. However, few report taking further action, including one in seven (14%) who have contacted an elected official by phone, mail, internet, or in person to discuss the cost of health insurance and one in nine (12%) who have posted on social media about the cost of health insurance.

Democrats are more likely than Republicans to say they have contacted an elected official (17% vs. 10%) or have posted on social media about the cost of their coverage (16% vs. 7%).