Berkshire Hathaway’s chief executive had the unusual task of reporting lower 2025 underwriting and investment income for GEICO and other insurance and reinsurance operations in his first report to investors recently.

After two years of rising underwriting profits, Greg Abel, taking the helm from Warren Buffett, addressed the state of the conglomerate’s insurance and reinsurance operations, which remained profitable but showed shrinking levels of underwriting income and higher combined ratios in all sectors—personal lines, commercial lines and reinsurance—in a letter to shareholders opening the annual report on Saturday.

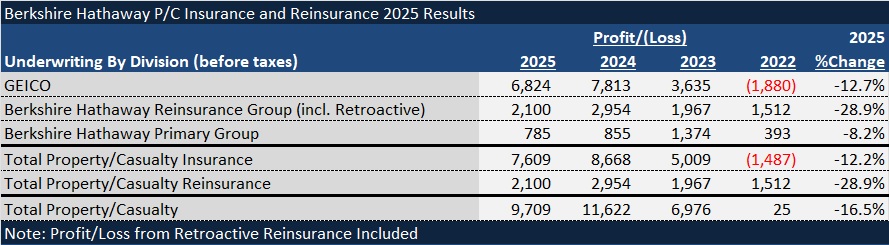

Personal lines insurer, GEICO, the largest in the group, accounted for more than 50% of the $1.9 billion year-over-year drop in pretax underwriting profits reported for the Berkshire property/casualty units overall. On a percentage basis, across all the P/C operations, pretax underwriting profits fell 16.5% to just over $9.7 billion.

Abel also highlighted slowing growth, warning this is likely to continue into 2026 for the P/C units as well.

“GEICO’s broad rate increases in recent years have restored margins but come at the cost of lower retention,” Abel wrote in one of his introductory remarks on P/C insurance performance.

“Competitors’ rate reductions may extend that pressure into 2026.”

“The GEICO team remains focused on pricing risks correctly for both existing and new customers. Restoring retention while maintaining underwriting discipline will take time,” he advised.

“Insurance will continue to be our core. While its performance will ebb and flow with capital conditions in the industry—perhaps dramatically—that heart of Berkshire will only grow stronger over time, reflecting the structural advantages that define it.”

Greg Abel, CEO, Berkshire Hathaway

As for commercial primary insurance operations, Abel reported that while “demand entering 2025 was solid, and pricing in most commercial insurance business segments was adequate or improving,” lower pricing or decelerating rate hikes were evident as the year progressed and more capital entered the market.

“We have always prioritized underwriting discipline over volume, and as pricing became less attractive, our premium growth plateaued,” he wrote.

“We expect these primary insurance businesses to face continued headwinds in 2026, and potentially beyond.”

Reporting “similar dynamics” for the reinsurance business—in particular, significant increases in available capital from both the traditional and alternative markets—Abel also highlighted the “more benign reinsured catastrophe loss burden in 2025 in most major regions” that fueled significant property reinsurance price drops.

“In most casualty reinsurance segments, claims inflation continued to outpace pricing,” he added.

“As long as these phases of the cycle endure, we expect to write less reinsurance premium,” he said.

GEICO: Lower Retention; Higher Combined Ratio

GEICO may have made up for lost customers with new ones, the Management Discussion and Analysis section of the annual report suggests, attributing 5.3% increases in GEICO’s written and earned premium levels last year to increased policies in force. The filing did not, however, disclose the magnitude of year-over-year PIF growth.

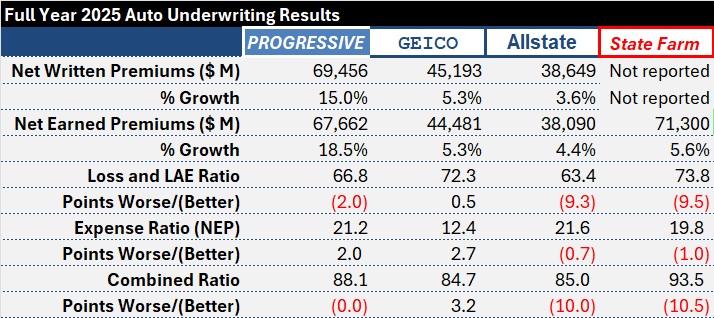

Unlike competitors, State Farm, Progressive and Allstate, which reported improvements in loss and loss adjustment expense ratios ranging from 2 points to almost 10 points in 2025, GEICO’s loss and LAE ratio worsened slightly, according to the annual report.

The 0.5-point loss ratio increase in 2025 reflected the impact of higher average claims severities, partially offset by an increase in average earned premiums per policy, lower catastrophe losses and a comparative increase in favorable development of prior accident years’ claims estimates,” the text if the Berkshire MD&A explains. (Takedowns in loss and LAE for prior accident years totaled $957 million in 2025, compared to $550 million in 2024.)

Giving more specifics about auto loss costs components, the filing notes that private passenger auto claims frequencies for property damage and collision coverages declined in 2025 vs. 2024 by 1-3%, while bodily injury frequency rose 4-6%. Severities rose across the board with BI average claims severity jumping 12-14% while PD and collision severity rose 2-4%.

Expenses and Staffing

Higher advertising and other policy acquisition expenses pushed GEICO’s expense ratio up 2.7 points to 12.4 in 2025.

Still, compared to its competitors, GEICO maintains an expense ratio advantage of 7-9 points, even though GEICO is also investing in technology, according to Abel.

“Alongside retaining its customer base with a more nuanced pricing strategy, GEICO is investing in technology to improve efficiency and service, while preserving its position as the industry’s low-cost provider,” he wrote in his letter to shareholders.

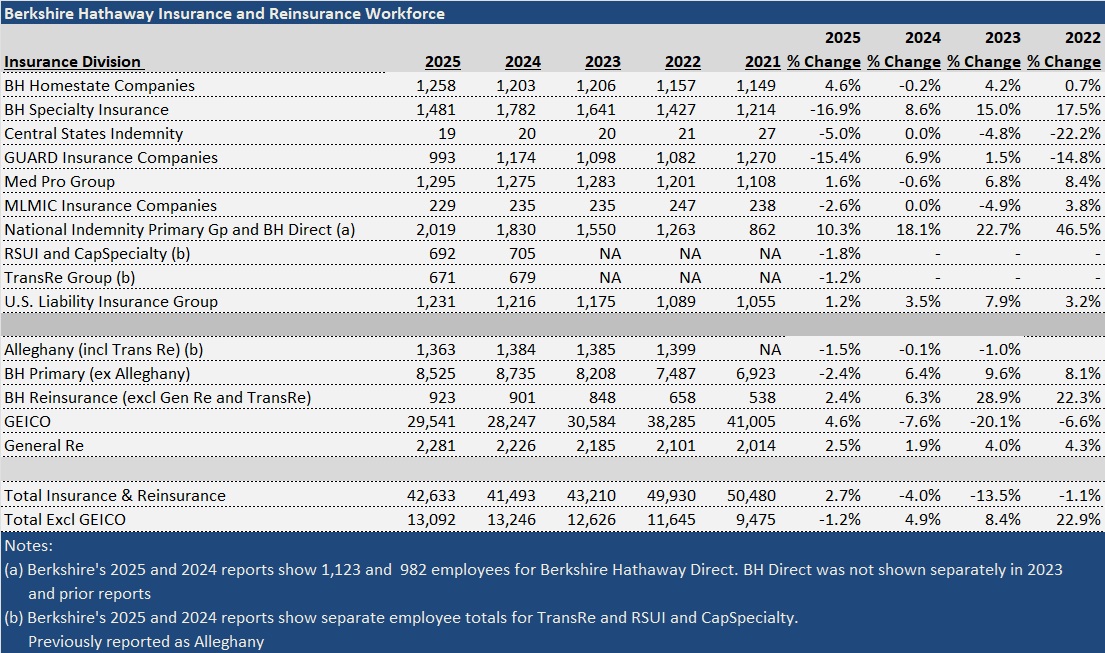

In past years, GEICO deepened its expense ratio advantage with staff cuts that brought its underwriting expense ratio down below 10 in 2023 and 2024. After trimming staff by 20 percent in 2023 and 8% in 2024, GEICO’s workforce grew nearly 5% 2025, marking the first increase since 2020, according to records maintained by Carrier Management from prior annual reports.

Related articles: GEICO’s ‘Eye-Popping’ 2023 Insurance Profits, Falling Employee Counts ; Staff Cuts Help Fuel GEICO Profit; Not ‘Pouring Money’ Into AI: Jain

In spite of staff growth last year, however, GEICO’s 2025 employee count of 29,541 remained 30% below the 42,000-plus employee count recorded five years earlier.

For the most part, employee counts for Berkshire’s insurance operations other than GEICO fell in 2025, compared to 2024. Notable exceptions were Berkshire Hathaway Direct, growing staff count by more than 14%, and National Indemnity Primary Group, up 6%. Berkshire also reported staff growth of roughly 2.5% in its reinsurance operations.

Less Underwriting Profit Across the Board

While GEICO had the biggest drop in underwriting profit in dollars last year, underwriting profits declined for all reporting segments included in the annual report. Berkshire’s reinsurance operations suffered the biggest percentage drop (32%, including life reinsurance operations, 29% excluding them).

Still, Abel highlighted the fact the overall combined ratio fell 13 points below breakeven (excluding retroactive reinsurance business for which Berkshire does not receive regular premiums).

Wrote Abel: “We produced a combined ratio of 87.1 across our property and casualty businesses in 2025, comparing favorably with our five-year average of 90.7, 10-year average of 93.0 and 20-year average of 92.2, an exceptional underwriting result for an insurer of our scale.”

On the top line, the MD&A attributed the $1.7 billion drop in P/C reinsurance premiums written that brought the total down to $20.2 billion—a decline of roughly 8%—to volume reductions in property business, which were in turn attributable to increased competition and lower rates.

As for commercial insurance operations, premiums and combined ratios changed only slightly in 2025 overall—with written premium declining less than 1% to $18.7 billion and the combined ratio moving up to 95.8 in 2025 from 95.4 in 2024.

Individually, the Berkshire Hathaway 2025 annual report provided these details about written premium growth for those separately managed insurance businesses:

- Premiums for health care liability insurer MedPro grew 9.0%, (primarily from student health business).

- Berkshire Hathaway Homestate Group, offering workers compensation, commercial auto and commercial property coverages, reported 7.4% premium growth.

- NICO Primary and Berkshire Hathaway Direct grew premiums by double-digits—13.0% for NICO Primary, mainly for commercial automobile business), and 15.8% for BH Direct, which writes commercial insurance for small and medium-sized businesses.

- Specialty insurer USLI saw premiums rise by 4.9%.

- GUARD, which like BH Direct targets small and medium-sized business customers but does so through independent agents, wholesalers and MGAs rather than direct platforms had the biggest premium decline in 2025—a nearly 33% drop. Berkshire reported that initiatives to exit unprofitable lines and tighten underwriting standards in the business owners, workers comp and personal lines products explained the decline.

- Specialty insurers in Berkshire’s RSUI Group saw premiums dip nearly 9%, with reduced property volumes explaining that drop.

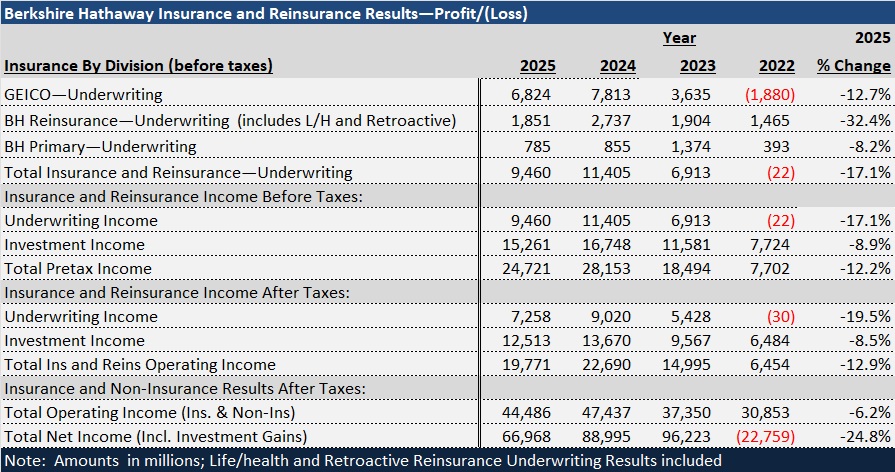

Another source of insurance revenue declined as well—investment income, which fell nearly 9 percent before taxes.

After taxes, underwriting and investment income across all of Berkshire’s insurance operations fell 12.9% to $19.8 billion.

Operating income for insurance and non-insurance operations fell 6% to $44.5 billion.

On the bottom line, including gains and losses from sales of investments and accounting for other-than temporary impairments of several investments, Berkshire reported $67 billion on net income for 2025, down 24% from $80 billion in 2024.

“Insurance will continue to be our core. While its performance will ebb and flow with capital conditions in the industry—perhaps dramatically—that heart of Berkshire will only grow stronger over time, reflecting the structural advantages that define it,” Abel wrote in his letter to shareholders. He highlighted structural strengths of Berkshire that allow underwriters and managers to remain patient across cycles, including:

- Significant capital, enabling them to underwrite large and unusual risks.

- The autonomy that managers have to run their businesses, and the absence of quarterly targets or growth mandates “that might otherwise distort their underwriting judgment.”

- “We insist on underwriting discipline as the most important ingredient in insurance success,” he added.

Finally, Abel wrote, “We focus on the long term, resisting temporary industry enthusiasms and exuberances.”

“The environment ahead will reward insurers whose focus remains on growing underwriting profit sustainably, not volume; customer trust and loyalty, not temporary spikes in market share; and long-term resilience, not short-lived opportunism,” he wrote.

Featured image: Greg Abel, May 5, 2018. (AP Photo/Nati Harnik)