and Federal Efforts at Regulation")

This brief, originally published on December 18, 2025, was updated on February 9, 2026, to reflect the PBM-related provisions that were enacted in February 2026.

The price of prescription drugs in the U.S. continues to be a concerning issue to the public, with KFF polling consistently showing the public supports various approaches to lowering prescription drug costs. Efforts to rein in drug costs have long been a priority for both federal and state policymakers. The Trump administration has recently taken steps to address drug costs through various administrative and regulatory actions, including multiple voluntary pricing agreements with drug manufacturers, the launch of the TrumpRx direct-to-consumer drug website, and CMS Innovation Center Models to bring ‘Most Favored Nation’ pricing to consumers in the U.S., though the impact and savings from these efforts are not yet known. During the Biden administration, Congress enacted the Inflation Reduction Act of 2022, which authorized the federal government to negotiate lower drug prices with manufacturers for some drugs covered by Medicare, among other provisions, resulting in an estimated reduction in the federal deficit of $237 billion over 10 years for the drug pricing provisions alone.

One player in the system of pharmaceutical pricing in the U.S. that has come under increasing scrutiny in recent years is the pharmacy benefit manager, or PBM. These so-called ‘middlemen’ are used by health insurance companies and self-insured employer plans to manage their pharmacy benefits. PBMs have been the focus of attention from policymakers for several reasons, including their business practices, market consolidation, and lack of transparency, all of which factor into concerns that PBMs themselves have played a role in increasing drug prices, even as they work to manage pharmacy benefits and costs for insurers.

In February of 2026, Congress enacted several PBM-related provisions in H.R.7148, the Consolidated Appropriations Act, 2026. This legislation includes provisions that will delink PBM compensation in Medicare Part D prescription drug plans from the price of a drug or rebate arrangements. It also requires PBMs to pass through 100 percent of rebates to employer health plans, and increases oversight of PBM services for Part D plans and employer health plans through transparency and data reporting requirements.

Separately, the Trump administration issued a proposed rule to require greater transparency from PBMs regarding their compensation in service contracts and arrangements with self-insured group health plans. This rule follows from an April 2025 Executive Order from the Trump administration directing the Assistant to the President for Domestic Policy to reevaluate the role of ‘middlemen’ to “promote a more competitive, efficient, transparent, and resilient pharmaceutical value chain”.

This brief provides an overview of the role of PBMs in managing pharmacy benefits, discusses federal efforts to reform certain PBM business practices, and explains the estimated federal budgetary impact of the recently enacted legislation, which would be a reduction in the federal deficit of $2.1 billion over 10 years, according to CBO. (This brief focuses on actions at the federal level and does not address state legislative efforts related to PBMs, which have occurred in all 50 states.)

The Role of PBMs

Pharmacy benefit managers (PBMs) act as intermediaries between drug manufacturers and insurance companies that offer drug benefits to employer health plans, Medicare Part D prescription drug plans, state Medicaid programs, and other payers. In this role, PBMs serve several functions: negotiating rebates and price discounts with drug manufacturers, processing and adjudicating claims, reimbursing pharmacies for drugs dispensed to patients, structuring pharmacy networks, and designing drug benefit offerings, which includes developing formularies (lists of covered drugs), determining utilization management rules, and establishing cost-sharing requirements.

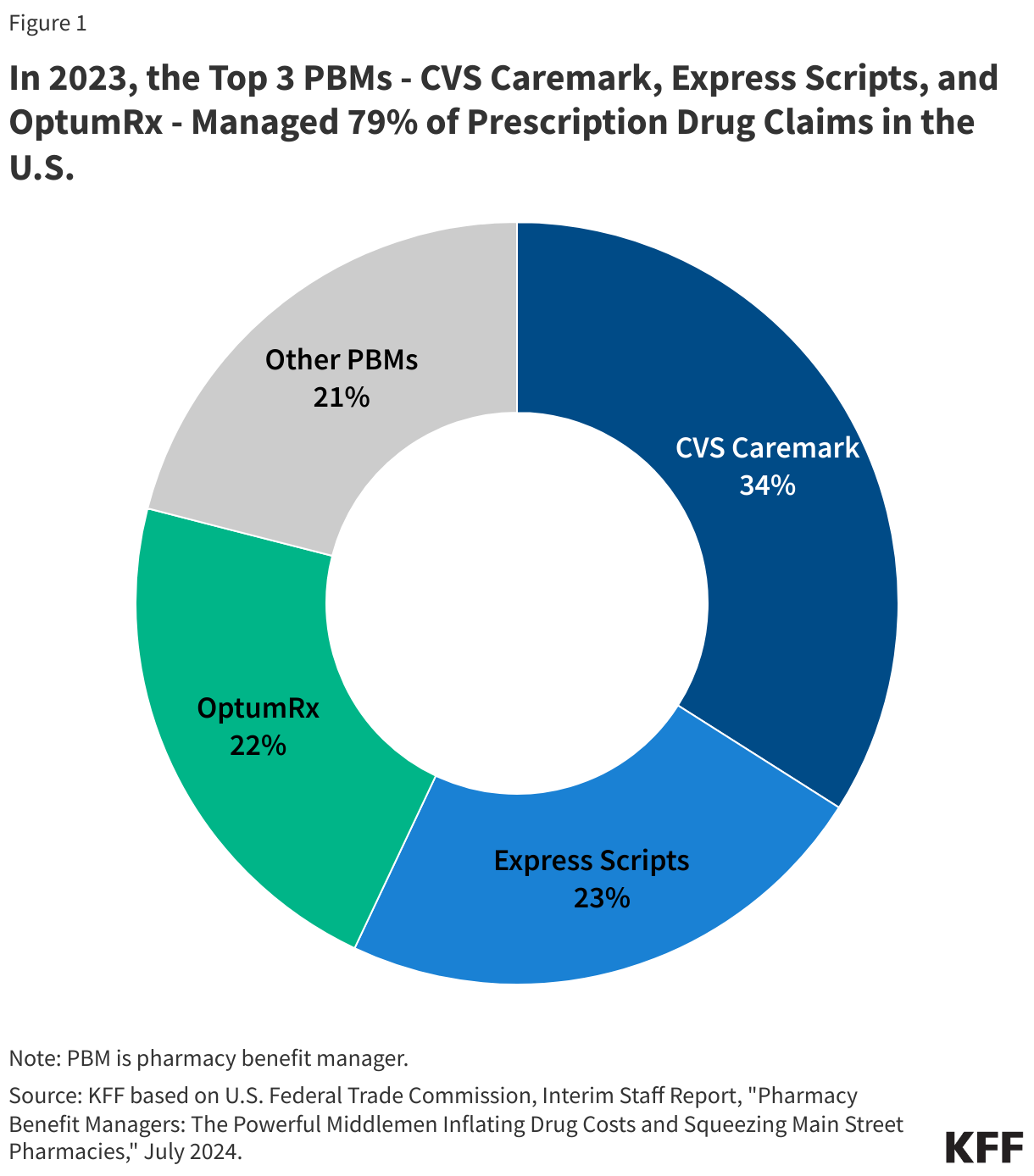

Although there are many PBMs, a few companies dominate the overall U.S. market. According to the Federal Trade Commission (FTC), the top 3 PBMs – OptumRx (owned by UnitedHealth Group), Express Scripts (owned by Cigna), and CVS Caremark (owned by CVS Health, which also owns Aetna) – manage 79% of prescription drug claims on behalf of 270 million people in 2023 (Figure 1).

Certain PBM Business Practices Have Given Rise to Concerns About Their Impact on Drug Prices

Sources of revenue: PBMs generate revenue in different ways. PBMs are typically paid fees for the functions they serve managing pharmacy benefits. PBMs also negotiate rebates with drug manufacturers in exchange for preferred placement of rebated drugs on a health insurance plan formulary, and they may retain a portion of the drug rebates they negotiate, though this may be more common in the commercial employer market than in the Medicare Part D market. Many state Medicaid programs and Medicaid managed care plans also contract with PBMs to manage or administer pharmacy benefits, including negotiating supplemental prescription drug rebates with manufacturers.

Rebates can help lower the cost of drug benefits for health insurance plans, which enables them to offer lower premiums in turn and may translate to lower out-of-pocket costs for patients at the point of sale. In order for PBMs to maximize rebate revenue, however, they may favor higher-priced drugs with higher rebates over lower-priced drugs with low or no rebates in their negotiations with drug companies. This may have an inflationary effect on drug pricing by manufacturers, increase costs for payers across the system, and raise out-of-pocket costs for patients who pay based on the list price – a particular concern for those without insurance but also for those with high-deductible insurance plans or when cost sharing is calculated as a percentage of the drug’s price, which is typical for higher-cost specialty drugs.

Because of these impacts, some have suggested that rebates negotiated between PBMs and drug manufacturers should be passed along in full to individuals at the point of sale and make discounts available upfront at the pharmacy counter. This arrangement would produce savings for individuals who take drugs with high rebates, since they would face lower out-of-pocket costs on their medications when they fill their prescriptions. However, if rebates are no longer being used to reduce a plan’s overall drug benefit costs, point-of-sale drug discounts could result in higher premiums for all plan enrollees.

Spread pricing: Another potential source of revenue for PBMs comes from the contracting practice of spread pricing, which is when a PBM pays a lower rate for a drug to the dispensing pharmacy than the amount the PBM charges an insurer for that drug and retains the difference or “spread” as profit. The practice of spread pricing can result in higher costs for insurers, while lower reimbursement levels put financial pressure on pharmacies.

PBMs have come under bipartisan scrutiny in recent years for spread pricing arrangements in Medicaid managed care that have increased Medicaid costs for states and the federal government. As a result, a number of states have prohibited spread pricing or adopted other reforms to increase transparency and improve oversight. Concerns about Medicaid spread pricing also led the Centers for Medicare & Medicaid Services (CMS) to issue an informational bulletin in May 2019 about how managed care plans should report spread pricing, which may have reduced the practice.

Consolidation: Consolidation in the PBM market has enabled a few PBMs to gain significant market power. As mentioned above, three PBMs manage nearly 80% of all prescription claims in the U.S. Moreover, the top three PBMs are vertically integrated with major health insurers: OptumRx is owned by UnitedHealth, Express Scripts is owned by Cigna, and CVS Caremark is owned by CVS Health, which also owns Aetna. Each of these PBMs also own mail order pharmacies and specialty pharmacies.

The FTC and members of Congress on both sides of the aisle have raised concerns that this level of market concentration and vertical integration enables PBMs to steer consumers to their preferred pharmacies, mark up the cost of drugs dispensed at their affiliated pharmacies, reimburse PBM-affiliated pharmacies at a higher rate than unaffiliated pharmacies for certain drugs, and apply pressure over certain contractual terms, all of which may disadvantage unaffiliated and independent pharmacies, contributing to pharmacy closures.

Transparency: Financial contracts between PBMs and drug manufacturers, including drug pricing information and the rebate arrangements that PBMs negotiate with drug manufacturers, are generally not made public. This means that plan sponsors often do not have insight into how much PBMs are actually paying for drugs on their formularies, and PBMs often consider this information to be proprietary. In the pharmaceutical supply chain as whole, many players operating in this market do not have information about prices, which can make informed decision-making difficult and imperfect.

Federal Efforts to Regulate PBMs

In February 2026, Congress enacted legislation that will address some PBM business practices, including:

- Delinking PBM compensation from the price of a drug, or any rebates or discounts that they negotiate for drug plans under Medicare Part D and instead basing compensation on a ‘bona fide service fee’, which will be a flat dollar amount that reflects the fair market value of services provided by PBMs, beginning January 1, 2028.

- Establishing transparency and reporting requirements for PBMs that provide services to Part D plans. This will include data on utilization, pricing, and revenues for formulary covered drugs; PBM-affiliated pharmacies; contracts with drug manufacturers; and other PBM business practices. This provision requires PBMs to provide this data to Part D plan sponsors as well as the HHS Secretary on an annual basis, no later than July 1 of each year, beginning July 1, 2028.

- Assuring pharmacy access for Medicare beneficiaries. This provision reinforces existing regulatory requirements that Part D plan sponsors contract with any willing pharmacy that meets their standard contract terms and conditions and have those conditions be ‘reasonable and relevant.’ These conditions will be defined and enforced beginning January 1, 2029, according to standards determined by the Secretary of Health and Human Services (HHS) no later than April 2028.

- Allowing for increased oversight of PBMs that provide services to employer health plans through data transparency and reporting requirements. This provision requires PBMs to report detailed prescription drug utilization and spending data to most employer health plans, including gross and net spending, out-of-pocket spending, pharmacy reimbursement, and other details related to the plan’s pharmacy benefit, effective for plan years beginning 30 months after the date of enactment. PBMs must also provide summary documents with certain information to plan participants upon request. PBMs are subject to civil monetary penalties for failing to meet reporting requirements.

- Requiring PBMs to fully pass through 100 percent of drug rebates and discounts to employer health plans regulated under the Employee Retirement Income Security Act of 1974 (ERISA). This includes private employer health coverage, both insured and self-insured. It would not apply to governmental plans such as state and local employee health plans or the Federal Employee Health Benefit Plan. This provision also expands the definition of ‘covered service provider’ under ERISA to include additional service providers, including PBMs and third-party administrators, requiring them to disclose information about direct or indirect compensation to plan fiduciaries.

- Requiring studies and reports on pharmacy benefit managers and the prescription drug supply chain in Medicare Part D from independent agencies, including the Government Accountability Office (GAO) and the Medicare Payment Advisory Commission (MedPAC).

The recently enacted legislation does not include Medicaid-related PBM provisions that were included in other bills, reportedly due to concerns about cost impact. These Medicaid provisions included:

- Prohibiting spread pricing in Medicaid and instead basing payments on a ‘pass-through model’ in which payments made by a PBM on behalf of the State Medicaid program to the pharmacy would be limited to the drug ingredient cost and a professional dispensing fee.

Separately, in January 2026, the Department of Labor (DOL) issued a proposed rule to require PBMs and other affiliated providers of brokerage or consulting services to disclose information about direct or indirect compensation they receive to plan fiduciaries of self-insured group health plans. This includes information about rebates or other payments from drug manufacturers, spread pricing arrangements, and payments received from pharmacies. The DOL estimates that for years 2026-2034, the rule provides benefits in the form of improved medication adherence and reduced healthcare utilization ranging from $74.5 million to $746.2 million annually; transfers in the form of reduced prescription drug prices of $108.8 million to $1.1 billion annually; and costs of $117.7 million annually incurred by self-insured group health plans and PBMs.

In February 2026, the FTC secured a settlement with Express Scripts over its business practices, alleging that Express Scripts inflated insulin costs by pushing drug manufacturers to compete for formulary placement based on the size of rebates off the list price rather than net price, with Express Scripts retaining a portion of the inflated rebate. As a result, the high list prices of these drugs negatively impacted patients whose out-of-pocket payments were tied to the list price of the drug. As part of the settlement, Express Scripts has agreed to modify its business practices, including ensuring member out-of-pocket costs are based on the net price rather than the list price; delinking compensation from the list price of a drug; increasing transparency for plan sponsors, including reporting on the cost of each drug; and subject to legislative and regulatory changes, ensuring members receive the benefit of prices available through the TrumpRx website as well as counting member payments made on TrumpRx toward deductibles and out-of-pocket maximums. At the time of the TrumpRx website launch, however, discounted prices advertised on the site are only available for cash-paying patients and cannot be used with insurance. The FTC also has lawsuits pending with the two other largest PBMs – Caremark and Optum – alleging they engaged in similar conduct regarding insulin prices.

Budgetary Effects of PBM Legislation

In general, cost estimates from the Congressional Budget Office (CBO) have scored PBM provisions with relatively low savings to the federal government. In the time since Congress began debating various PBM reforms, certain PBM business practices may have evolved in ways that could blunt the potential spending impact of these efforts, unless those new practices are also specifically targeted.

For the PBM reforms in the recently-enacted appropriations law, CBO estimated a total federal deficit reduction of $2.12 billion over 10 years (2026-2035):

- A reduction of $444 million from delinking PBM compensation from the cost of medications for drugs under Part D and establishing PBM transparency and reporting requirements for Part D plans

- An increase of $188 billion from assuring pharmacy access and choice for Medicare beneficiaries

- A reduction of $1.865 billion from increasing oversight of PBMs that work with employer health plans, including $1.843 billion in additional revenues and savings of $22 million

For the provision to increase oversight of PBMs that work with employer health plans, a prior CBO estimate of this provision assumed that because insurers had more information about the operations of their PBMs, it would lead to a reduction in prescription costs, and therefore a modest reduction in premiums charged in the group health insurance market, though savings would likely diminish over time. Assuming there would be a reduction in premiums, this would increase wages and therefore increase federal revenues.

CBO did not provide an estimate for the provision that requires PBMs to pass through 100 percent of drug rebates and discounts (excluding service fees) to some employer health plans.