Consultancy Lane Financial LLC launches its new report on the catastrophe bond market with some good news, its analysis shows the outstanding market yield of non-impaired natural cat bonds is no longer as soft as it was at the end of 2025, but the firm also highlights that investor returns have been eroded by falling secondary market prices.

The outlook hasn’t changed a great deal, with Lane Financial sticking to its forecast of a 6% total return after an expected level of losses for cat bonds in 2026.

But, the situation has brightened somewhat, with the firm’s analysis perhaps suggesting a bottom in pricing terms has been reached, as yields ticked back up and multiples rose slightly.

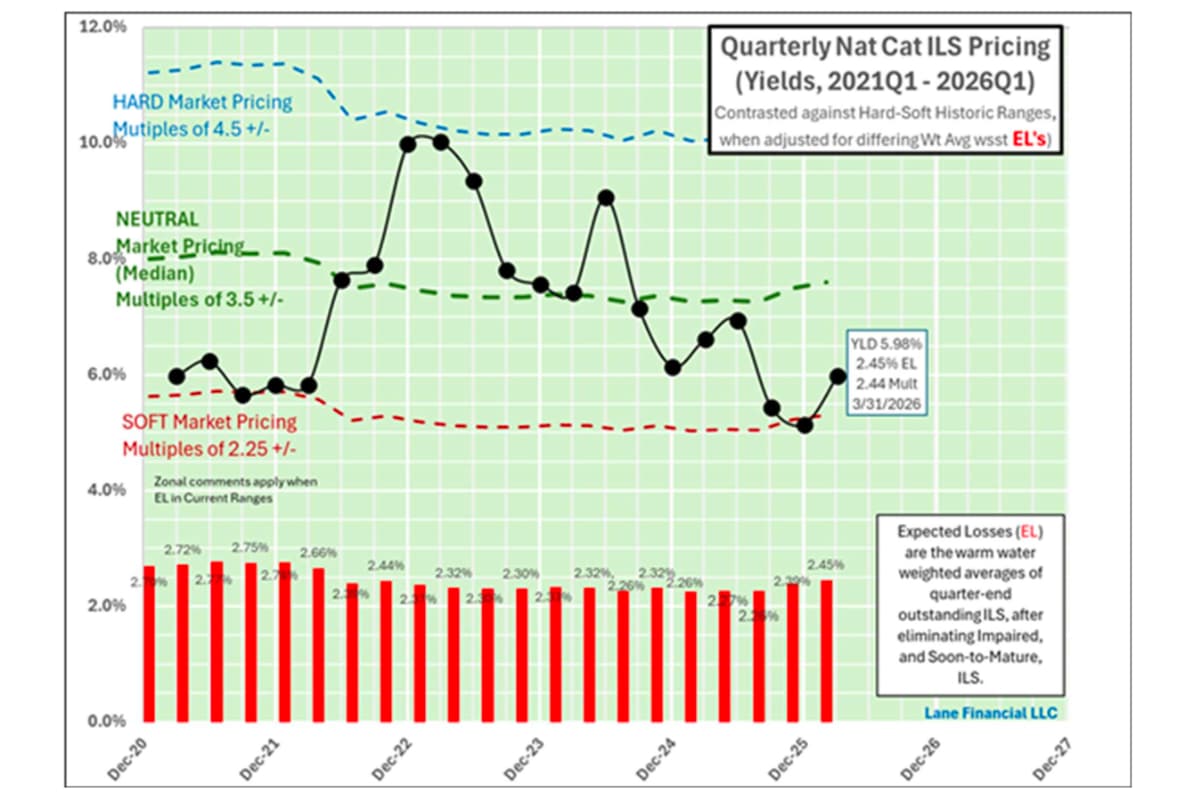

Lane Financial explains, “The good news is fairly simple. As the quarter-end yield chart shows, the outstanding, non-impaired, Nat Cat ILS are no longer as soft as at the end of Q4 2025. Yields, the secondary market proxy for Rate-on-Line premium levels, are half-way back to the neutral zone.

“The yield on the outstanding set of ILS at each quarter-end has risen from 5.14% to 5.98% against a rise in the Expected Loss [EL] from 2.39% to 2.45%, a net gain in the underwriting margin of 0.77% (77 bps).”

Qualifying this by adding that, “This is good, but not great, news for investors in ILS. It is certainly better than seeing softer prices descend below the historical thresholds shown on the chart.”

Lane Financial’s chart can be seen below:

Similar pricing effects are visible in Artemis’ chart showing the average expected loss, spread and spread over EL at issuance for Q1 2026 catastrophe bonds.

While our chart showing the average multiple-at-market at issuance of cat bonds shows an increase for Q1 2026 as well, reflecting the slightly improved conditions and showing this good, but not great news extends to new cat bond issuance as well as yields across the outstanding market.

Lane Financial goes on to explain that there is bad news as well, as these higher yield effects result in lower pricing on outstanding cat bonds.

“As yields have risen, bond prices have fallen. The average bond price of the outstanding Nat Cat ILS at the end of 2025 was $102.9. Currently the average is $101.7. By this measure the investor has lost $1.2 points (120 bps) from his total return calculation. That represents a significant drag on first quarter underwriting results,” Lane Financial’s report explains.

But importantly add that, “The secondary market is saying, from here on the outlook is slightly better, but to get to this point the first quarter results have already been eroded below expectation.”

Which perhaps implies that an over-exuberant market towards the end of 2025 softened the picture more than was eventually deemed comfortably, resulting in a slight correction through Q1 2026 that provides the slightly better outlook for yields and ultimately returns. But typical seasonal spread widening will also be a factor here, given the time of year.

Of course, given the volatility experienced in financial markets and geopolitics, as well as perceived issues in areas of credit investments, you would not blame institutional investors and investment managers to have elevated their perceptions of the cost-of-their-capital as well, an often under-played dynamic which can affect securities based asset classes like catastrophe bonds.

On the risk-free return on collateral, Lane Financial note that given the man-made disaster of war on Iran and around the Middle East, the inflation outlook has shifted considerably and expectations are no longer for further interest rate reductions.

But, despite a chance of the risk-free rate now remaining stable, or even rising, Lane Financial says it stands with its prediction, “Expected Nat Cat ILS total returns for 2026 around 6.0%, net of losses being at expected levels.”

Lane Financial’s just-released paper also contains an interesting discussion on the use of multiple expected loss metrics (or not) in catastrophe bond secondary market pricing sheets.

You can download a copy of the new Lane Financial paper here.