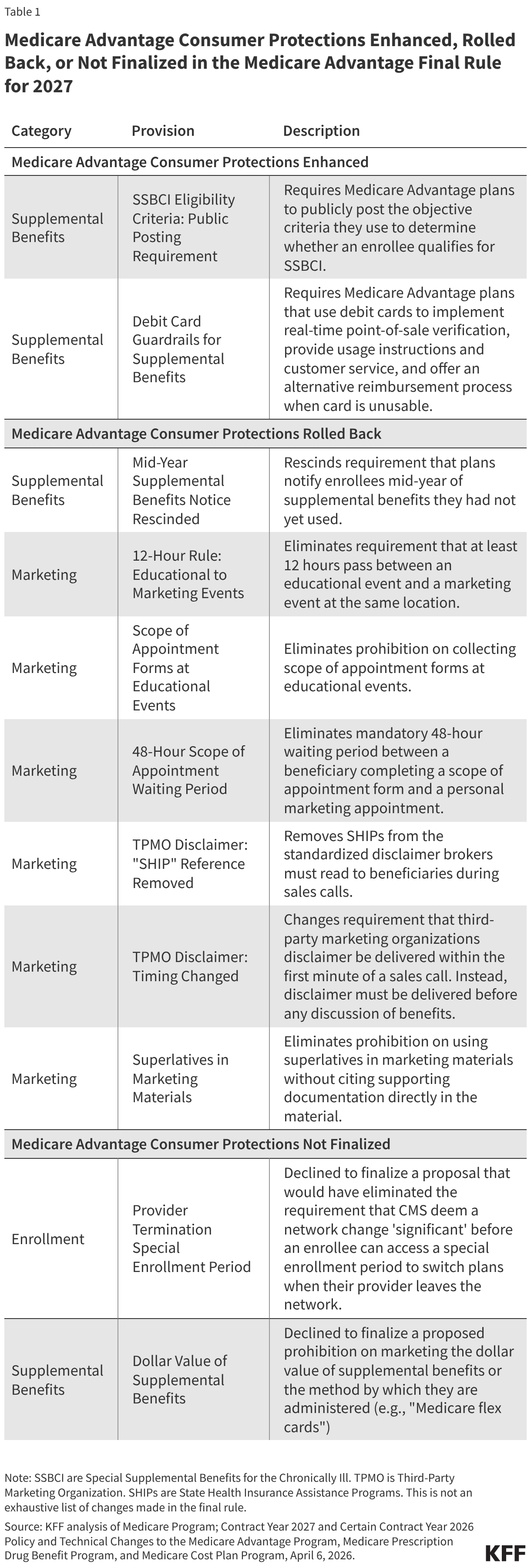

CMS recently finalized policies as part of the 2027 Medicare Advantage final rule that both enhance consumer protections and roll back changes to the Medicare Advantage program that were intended to protect consumers. These changes have gotten less attention than payment issues and changes to the star ratings system, which also affect plan payments, but could have implications for Medicare beneficiaries (See Table 1):

- CMS will enhance some consumer protections by requiring Medicare Advantage plans to post eligibility criteria for Special Supplemental Benefits for the Chronically Ill (SSBCI), making it easier for prospective enrollees to assess their eligibility for these benefits, which include food and produce, pest control, and transportation for non-medical needs, among others. CMS also added guardrails for debit cards issued by plans to administer supplemental benefits, so enrollees can better understand how to use these cards to obtain their benefits and also to prevent the purchase of non-covered items.

- CMS rolled back some changes to the Medicare Advantage program that were intended to protect consumers, including rescinding a requirement that plans notify enrollees of unused supplemental benefits mid-year, as well as eliminating a number of marketing requirements, such as provisions aimed at increasing the separation between marketing activities from educational events and a prohibition on the use of superlatives in marketing materials, and removes the State Health Insurance Assistance Programs (SHIPs) from the list of resources that brokers must offer to beneficiaries for further information during sales calls.

- In addition, CMS did not finalize a proposal that would have modified a special enrollment period to make it easier for enrollees to switch coverage if one of their providers is no longer part of their Medicare Advantage’s plan network.

CMS Finalized a Few Changes to the Medicare Advantage Program That Enhance Some Consumer Protections

Improving SSBCI Eligibility Transparency. Medicare Advantage plans offer supplemental benefits to Medicare Advantage plan enrollees, such as dental, vision, and hearing, which are considered primarily health related (e.g., preventing or treating an illness). Beginning in 2020, Medicare Advantage plans have also been able to offer supplemental benefits that are not primarily health related for chronically ill beneficiaries, known as Special Supplemental Benefits for the Chronically Ill (SSBCI). These benefits include food and produce, general supports for living (i.e. assistance with housing and utilities), pest control, and transportation for non-medical needs, among others. To receive these benefits, Medicare Advantage enrollees must have one or more comorbid and medically complex chronic conditions that meet all of the following criteria:

- is life threatening or significantly limits the overall health or function of the enrollee;

- has a high risk of hospitalization or other adverse health outcomes; and

- requires intensive care coordination.

Additionally, Medicare Advantage plan must determine that the benefit has a reasonable expectation of improving or maintaining the health or overall function of the chronically ill enrollee.

The final rule requires Medicare Advantage plans to post on their websites the eligibility criteria they use to determine whether an enrollee qualifies for SSBCI to increase transparency for potential enrollees, including both the criteria for meeting the “chronically ill” definition as well as the specific criteria for each benefit. Previously, plans were not required to post eligibility criteria publicly. CMS noted that in response to a prior rule, they had received many comments requesting that plans post their specific SSBCI criteria on a public-facing website. CMS expects this change will provide greater transparency for Medicare Advantage enrollees and improve their ability to assess whether they are eligible for these benefits and make an informed decision when they are deciding whether to enroll in a plan.

Moreover, CMS added regulatory language to ensure plans apply the eligibility criteria to Medicare Advantage enrollees in an objective and consistent manner. The rule clarifies that Medicare Advantage plans must verify all statutory criteria for “chronically ill” status through an objective process such as a health risk assessment or a claims review, rather than allowing self-attestation alone.

Enhancing Guardrails for Debit Cards that Administer Supplemental Benefits. Medicare Advantage plans are permitted to use debit cards to administer supplemental benefits, such as helping cover the cost of dental or vision services, the purchase of over-the-counter products, or the purchase of food and produce at participating retailers. CMS requires that Medicare Advantage plans administer these benefits in a way that ensures the debit card only be used towards plan-covered items and services. CMS noted, however, that enrollees frequently express confusion about what can be purchased with their plan debit card, and that stakeholders have raised concerns that these cards could be used to purchase items that are not covered by Medicare Advantage plans, particularly at large retailers. CMS also indicated that debit cards may be subject to fraud in the absence of stronger guardrails applied to non-covered items.

The final rule codifies existing regulations and adds requirements regarding the use of debit cards for supplemental benefits. Beginning in 2027, Medicare Advantage plans that choose to use debit cards to administer supplemental benefits must provide cards that are electronically linked to plan-covered benefits through a real-time identification mechanism that verifies eligibility at the point of sale. CMS states that real-time verification will ensure ease of access to benefits, increase transparency, and help eliminate fraud by preventing unauthorized purchases of non-covered items. Plans are also required to provide instructions to enrollees on how to use the debit card, provide customer support service to enrollees who have questions about how to use the debit card, and maintain an alternative reimbursement process for circumstances where enrollees are not able to use their debit card. CMS explained that it expects these changes will make Medicare Advantage enrollees more aware of their debit card benefits and how to use them.

The rule does not finalize a proposed change that would have prohibited marketing materials from listing the dollar value of supplemental benefits or the method by which these benefits are administered (e.g., debit cards or “Medicare flex cards”). In the proposal, CMS raised concerns with marketing tactics related to debit cards, including that some Medicare Advantage plans had been marketing the debit cards in inaccurate and misleading ways, using terms like “flex card” with an enticing dollar value attached to them, which might imply enrollees will automatically receive unrestricted spending money just by enrolling in the plan. However, CMS declined to finalize this proposal, citing concerns that this change would reduce informed decision-making before beneficiaries enroll in a plan.

CMS Also Rolled Back Changes to the Medicare Advantage Program That Were Intended to Protect Consumers

Mid-Year Supplemental Benefits Notice Rescinded. Medicare Advantage plans offer an array of supplemental benefits, but there is little data yet available to examine how frequently enrollees are using the benefits available to them. Medicare beneficiaries often highlight the availability of extra benefits as a reason they choose to enroll in Medicare Advantage plans, and CMS has also observed beneficiaries make enrollment decisions on these benefits, but that enrollees are often unaware of the benefits available to them and are not using them. The April 2024 final rule required Medicare Advantage plans to send enrollees a mid-year notice, between June 30 and July 31 of each plan year, listing any supplemental benefits the enrollee had not yet used during the first six months of the year, which was set to take effect January 1, 2026.

CMS rescinded this requirement before it took effect, citing several reasons: more recent survey data showing that 70 percent of Medicare Advantage enrollees reported using at least one supplemental benefit in the past year, which CMS suggests means beneficiaries are aware of these benefits, (though CMS notes there are still data gaps on utilization of these benefits); the administrative and financial burden on plans, particularly on smaller Medicare Advantage plans; and that this information is duplicative of information in the Annual Evidence of Coverage document that is already sent to enrollees. They also note this recission is consistent with the administration’s priorities to reduce unnecessary regulatory burdens, laid out in its Executive Order, Unleashing Prosperity Through Deregulation.

Marketing Requirements Rolled Back. CMS regulates how Medicare Advantage insurers, as well as agents, brokers, and other third parties who sell Medicare Advantage plans may communicate with beneficiaries. In recent years, CMS has documented patterns of aggressive and misleading marketing behavior, based on reports from state insurance commissioners, State Health Insurance Assistance Programs (SHIPs), and beneficiary advocacy groups, and has made a number of changes in prior rules to provide additional oversight of Medicare Advantage plan marketing. The recent final rule eliminates many of these provisions, with the stated goal of streamlining regulatory requirements for agents and brokers, and making the services offered by these groups more accessible to beneficiaries.

- Limitations on Marketing at Educational Events Rolled Back: CMS requires that Medicare Advantage insurers, agents, and brokers clearly distinguish between educational and marketing events, and prohibits the discussion of specific plan costs or benefits at events promoted as educational. The April 2023 final rule reinforced this separation by prohibiting the collection of scope of appointment forms at educational events, requiring a 48-hour waiting period between the collection of scope of appointment forms and personal marketing appointments, and requiring a 12-hour waiting period between educational and marketing events at the same location. These provisions were intended to prevent beneficiaries from feeling pressured into attending marketing events or making coverage decisions on the spot when seeking out educational information.

The current final rule rolls back these provisions, citing stakeholder feedback that waiting periods create unnecessary delays and may be burdensome to beneficiaries who must travel for multiple events and appointments that could otherwise take place in a single session. Agents and brokers may now collect scope of appointment forms at educational events, and may conduct a personal marketing appointment at any point afterwards, with no waiting period. Further, educational and marketing events may now be held back-to-back in the same location, provided that beneficiaries are notified of the transition and offered the opportunity to leave if they prefer. CMS noted that some commenters opposed these changes due to concern that they may leave beneficiaries more vulnerable to aggressive sales tactics and may blur the line between educational and marketing information.

- Prohibition on Use of Superlatives in Marketing Materials Eliminated: The final rule eliminates certain requirements around the language used in marketing materials, such as a prohibition on the use of superlatives (e.g., “best” or “most”) without supporting documentation. CMS first introduced this requirement in the April 2023 final rule, citing concern that these claims may be misleading when taken out of context, and may encourage beneficiaries to enroll in a plan based on information that is misrepresented or misunderstood. The current rule revises this stance, stating that existing CMS requirements already prohibit the use of misleading or inaccurate claims in marketing materials, while the prohibition on superlatives represents an undue burden for insurers, agents, and brokers that does not meaningfully expand on these other protections.

- Mandatory Disclaimer Requirements Modified: CMS requires that brokers and other third parties who represent multiple Medicare Advantage insurers begin all sales calls with a mandatory disclaimer stating that they do not represent every plan available in the area and providing beneficiaries with a list of resources they may reach out to for further information. CMS introduced this requirement in the May 2022 final rule to ensure that beneficiaries had access to complete, unbiased information about their coverage options, as many brokers only represent a subset of available plans and may have a financial incentive to steer beneficiaries towards some plans over others. The current final rule preserves this requirement, but allows the disclaimer to be provided later in the call as long as it is stated before any discussion of specific plan benefits, rather than in the first minute of the call as previously required.

Notably, the rule also removes the State Health Insurance Assistance Programs (SHIPs) from the list of resources that must be included in the disclaimer, now limited to official CMS resources such as 1-800-MEDICARE and Medicare.gov. SHIPs are federally-funded, state-based programs that offer free, unbiased counseling and education to Medicare beneficiaries. This change prompted criticism from some commentors, who noted that 1-800-MEDICARE is not generally equipped to provide the same level of in-depth counseling or local information that SHIP counselors are trained to provide. However, CMS states that SHIP volunteers may not always have the expertise to help beneficiaries navigate increasingly complex Medicare Advantage options and that the standardized training and 24/7 availability of customer service representatives at 1-800-MEDICARE make it a more appropriate resource in this context, while also noting that 1-800-MEDICARE may still refer callers to their local SHIP on a case-by-case basis.

CMS Declined to Finalize a Proposal to Streamline the Medicare Advantage Special Enrollment Period for Provider Terminations

Medicare Advantage plans have networks of providers, and beneficiaries must see providers in their plan’s network or potentially pay higher cost sharing. KFF analysis has shown that Medicare Advantage enrollees have access to about half of the physicians available to traditional Medicare beneficiaries in their area, on average. Medicare beneficiaries say having access to their preferred providers is an important factor when selecting their Medicare coverage. With this in mind, the Trump administration recently launched a new provider search tool on the Medicare plan finder to help beneficiaries identify if their doctors are in a plan’s network, though it experienced issues during its initial rollout.

While Medicare beneficiaries may select plans based on access to their preferred doctors and hospitals, providers can leave Medicare Advantage networks at any time during the year, potentially disrupting coverage for plan enrollees. Currently, a special enrollment period (SEP) for Significant Change in Provider Network allows Medicare Advantage enrollees to switch plans or return to traditional Medicare when CMS determines there were “significant” changes to their plan’s provider network – for example, the termination of a contract with a large hospital system. When CMS makes that determination, Medicare Advantage plans must send a separate notice to affected enrollees explaining their SEP eligibility to select different coverage, including guaranteed issue rights to purchase a Medigap policy regardless of pre-existing conditions.

CMS proposed to eliminate the significance determination, making the SEP available to any “affected enrollee” of a provider termination, defined as someone assigned to, currently receiving care from, or having received care within the past three months from a terminated provider. Rather than waiting for CMS to review and approve a significance finding, plans would include SEP eligibility information in the standard provider termination notice already sent to enrollees. Enrollees could then attest directly to the plan that they meet the affected enrollee definition and are eligible for a special enrollment period to change their Medicare coverage.

This proposal would have put the decision in the hands of Medicare beneficiaries – allowing them to decide whether a provider termination was significant enough to warrant switching coverage, rather than waiting for that determination from CMS. However, CMS declined to finalize this proposal and did not explain its rationale for its decision. CMS does note that this topic generated broad interest and may be addressed in further rulemaking.