On June 1, 2026, the Centers for Medicare and Medicaid Services (CMS) issued a long-anticipated interim final rule that will guide state implementation of Medicaid work requirements. The 2025 reconciliation law requires 44 states to condition Medicaid eligibility for adults in the Affordable Care Act (ACA) Medicaid expansion group and enrollees in certain waiver programs, including in non-expansion states (Georgia, Tennessee, and Wisconsin), on meeting work requirements starting January 1, 2027, or sooner at state option. The law specifies mandatory exemptions, including individuals who are “medically frail.” Given the abbreviated implementation timeline, states had tentatively moved forward with key decisions over how to implement the medical frailty exemption even as they waited for formal guidance from CMS.

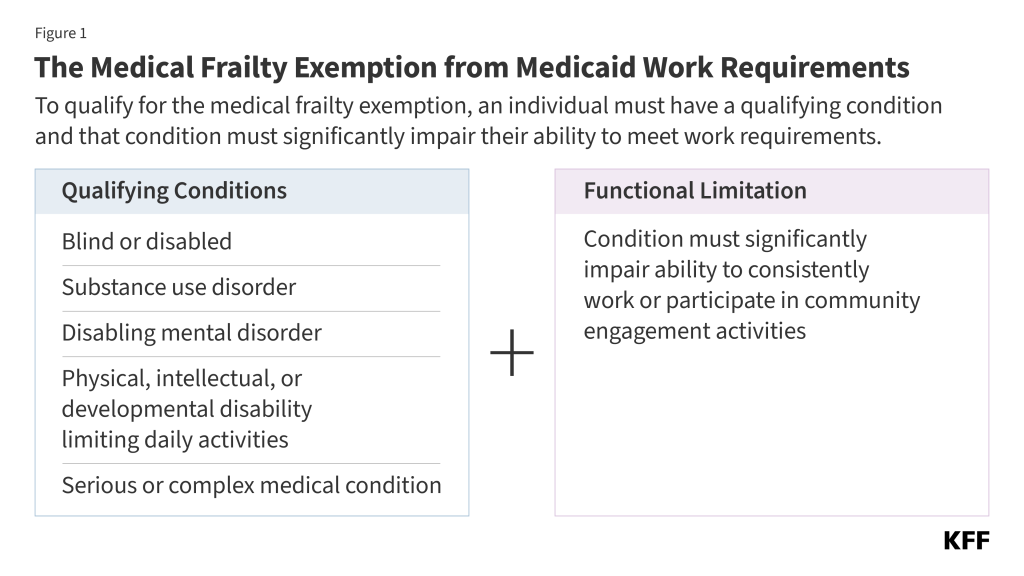

Significantly, the rule adopts a restrictive definition of medical frailty that differs from states’ early expectations and ties medical frailty to an individual’s ability to meet the community engagement requirements, including work or volunteer activities. The 2025 law specifies the medically frail exemption includes five categories of individuals who: are blind or disabled; have a physical, intellectual, or developmental disability that limits their ability to perform one or more activities of daily living (ADL); have a substance use disorder; have a “disabling” mental disorder; or have a “serious or complex” medical condition. The new rule requires states to consider not just whether the individual falls into one of the five categories described in the statute, but also whether the individual’s condition impairs their ability to engage in community engagement activities (including but not limited to work). States will likely need to pivot from earlier implementation plans and approaches to accommodate the new guidance.

States were already facing challenges in preparing to implement complex new requirements by January 1, 2027 and the provisions in the rule will amplify operational challenges, with added risks for states due to the potential for audits and financial penalties. The rule also may increase barriers for individuals to obtaining and maintaining coverage, leading to more people falling through the cracks and becoming uninsured. In addition, more complicated definitions of medical frailty may be difficult for states to explain as they conduct outreach with enrollees and potential applicants. This brief describes the new guidance and potential challenges states will face in operationalizing this exemption.

How Does the Interim Final Rule Define Medical Frailty?

For all categories of medical frailty, states are expected to develop a list of diagnosis and other codes to identify people who could potentially qualify for the exemption. States will be required to create lists of conditions that could potentially qualify someone as medically frail (generally in the form of health care code sets), which they must revise on a regular basis to reflect implementation experiences. CMS notes that the lists states use will be auditable, and if states are found to have determined an individual to be medically frail with little to no support for the conclusion that their physical, mental, or other behavioral health condition significantly impairs their ability to comply with the community engagement requirement, states would not be in compliance with the regulation and could be subject to financial penalties.

The rule relies heavily on existing definitions for the five medically frail categories and generally provides little additional clarification to help states develop the list of conditions for each category. In the rule, CMS said it did not believe it would be appropriate to include an exhaustive list of conditions in regulation, although they did provide examples of conditions across the various categories that could reasonably be expected to cause an individual to be medically frail. The rule acknowledges multiple existing definitions for several categories and ultimately defersto states the exact process of capturing individuals in these groups, explaining it “would be incredibly difficult to set one standard.” Notable details in the new rule include:

- In the case of individuals with an SUD, the rule clarifies that the medical frailty category applies regardless of whether they are in an active treatment program but does not include individuals who have been in active recovery for 5 or more years.

- For those with a serious or complex medical condition, the rule provides a new definition that requires a severe level of acuity for a condition to be considered serious or complex, which stands in contrast to other conceptions of “serious or complex” medical conditions that include individuals for whom maintaining access to health coverage is necessary to protect against serious health consequences if treatment is interrupted.

For all five categories, the rule makes clear that states must consider both if an individual’s condition meets the medical frailty definition and also if it significantly impairs their ability to work or engage in qualifying activities (Figure 1).

How Does the CMS Guidance Direct States to Verify Medical Frailty?

States are required to use claims and encounter data from the preceding 12 months to verify medical frailty status before requesting information from the individual; however, it will be difficult to use claims data alone to verify an individual’s ability to work. To ease the burden on individuals, the law directs states to use available information “where possible” to verify compliance with Medicaid work activities or exemption status, without requiring additional documentation from individuals. States are required to use claims or encounter data from the preceding 12 months as a data source. States are told they cannot consider information older than 12 months as this information “may not reflect the individual’s current condition.” The rule also encourages states to incorporate concise, plain language screening questions for use at application and renewal to identify individuals who may be medically frail. The rule is explicit that diagnosis alone cannot be used to verify medical frailty (because states must also consider whether an individual is sufficiently impaired from being able to work), limiting the ability of states to verify medical frailty on an ex parte (i.e., automatic) basis.

The rule does not provide details on criteria states should use for measuring severity of conditions or ability to meet new requirements. The rule only provides high-level examples of processes states may adopt to verify that an individual’s condition impairs their ability to work, such as algorithms that use administrative claims data to assign acuity scores, or using lists of qualifying diagnosis codes combined with utilization and other data. States may need to use combinations of data such as utilization data (e.g., hospitalizations), prescription drug data, and durable medical equipment (DME) prescription data. These approaches require states to implement even more complicated systems changes within the next six months that they were not anticipating based on earlier informal guidance. In addition, while these examples suggest states may be able to use acuity as a proxy for an individual’s ability to work, the rule is not clear on how states are expected to make these determinations. With the potential for audit, states may struggle to operationalize the medical frailty exemption in a way that protects them from financial penalty and minimizes administrative burden, without denying coverage to individuals who should qualify for the exemption.

Data limitations make it likely that medical frailty determinations will not be automated for many individuals. Examples of limitations include lack of data on file for new applicants and recent enrollees, or providers not consistently coding conditions or not using codes identified by the state. Certain individuals, such as those with functional limitations or behavioral health conditions, may also be more difficult to identify using claims data. States are also not provided with clear guidance on how to assess whether an individual is able to work or engage in community engagement activities, including what type of work activities states must consider. The more individualized the required assessment is, the more difficult it will be for states to auto-exempt individuals using data.

While states may need to rely on confirmation from treating providers to verify medical frailty conditions and ability to participate in community engagement activities, the rule offers little information on what information states need to collect from providers. States choosing to accept provider documentation are told that lists of who they choose to be allowable practitioner types must be shared with CMS if requested as part of oversight and data monitoring activities. Relying on provider confirmation could increase administrative burden (on the clinical workforce, individuals, and states), particularly for providers that treat large shares of Medicaid patients. Relying on providers or eligibility workers to determine whether an individual is able to work will likely require a subjective decision and could raise ethical concerns among providers. New Hampshire had previously implemented work requirements with a requirement that individuals needed to be deemed unable to work by providers to qualify for an exemption; enrollees with physical and behavioral health problems struggled when applying for exemptions, often because primary care providers resisted signing forms declaring that their patients were unable to work. Research also shows that physician attitudes to assisting patients who request exemptions from work requirements can vary substantially. In addition, because providers receive Medicaid payments and, therefore, have an interest in their patients maintaining health coverage, requesting information from them to confirm a medical frailty exemption could raise conflict of interest issues.

While states are permitted to use self-attestation to verify medical frailty, the rule limits reliance on self-attestation starting in January 2028. Given the limitations of existing data sources and the difficulty of identifying whether an individual is medically frail, accepting self-attestation of medical status or ability to work could relieve the administrative burden for states as well as applicants and enrollees. Acknowledging data limitations states face particularly for new applicants, the rule allows states to accept self-attestation throughout 2027 in cases where there is no reliable information available to the state. However, starting January 1, 2028, states may only accept self-attestation of medical frailty status one time during an individual’s enrollment period. States would then be expected to verify individuals using available data or require documentation or other information from individuals for future renewals.

The rule requires states to verify medically frail exemption status at least every 12 months. States must reverify medical frailty even for people whose health condition or disability status is unlikely to change every 12 months; however, the rule gives states the option to reverify medical frailty more frequently (such as at each 6-month renewal period). For states that elect to verify compliance between regular renewals (e.g., quarterly), the rule specifies that individuals identified as specified excluded individuals during their most recent verification, including those who meet medical frailty exemptions, are not subject to more frequent verifications.