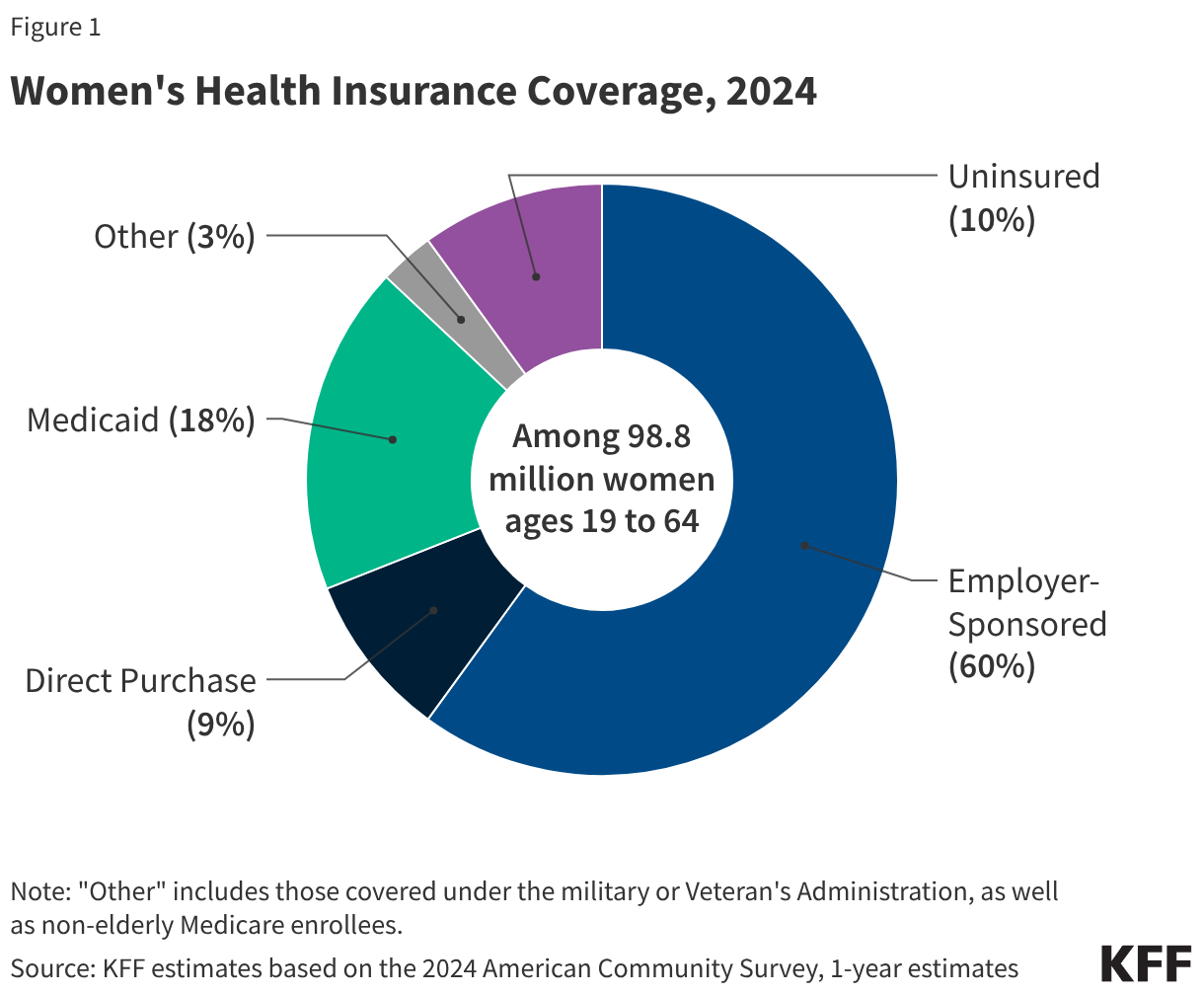

Approximately 59.7 million women ages 19-64 (60%) received their health coverage from employer-sponsored insurance in 2024 (Figure 1).2

- Women in families with at least one full-time worker are more likely to have job-based coverage (70%) than women in families with only part time workers (33%) or without any workers (16%).3

- In 2024, annual insurance premiums for employer sponsored insurance averaged $8,951 for individuals and $25,572 for families. Family premiums have increased 24% between 2019 and 2024. On average, workers paid 16% of premiums for individual coverage ($1,368) and 25% for family coverage ($6,296) with the employers picking up the balance.

Non-Group Insurance

The ACA expanded access to the non-group or individually purchased insurance market by offering premium tax credits to help individuals afford coverage purchased through state-based health insurance Marketplaces. It also included many insurance reforms to alleviate some of the long-standing barriers to coverage (such as gender rating, lack of maternity coverage, and pre-existing condition exclusions, having a disproportionate effect on women) that were common in the non-group insurance market prior to the ACA. In 2024, about 9% of women ages 19 to 64 (approximately 8.9 million women) and 9% of their male counterparts purchased insurance in the non-group market.4 This includes individuals who purchased private policies from the ACA Marketplace in their state, as well as those who purchased coverage from private insurers that operate outside of Marketplaces under similar rules.

- Most individuals who seek insurance policies in their state’s Marketplace qualify for assistance with the costs of coverage. Individuals with incomes below 400% of the Federal Poverty Level (FPL) ($65,280 for an individual under 65 in 2024) can qualify for assistance in the form of federal tax credits which lower premium costs.

- Enhanced federal subsidies that began as part of two COVID era bills that temporarily increased the amount of financial assistance already eligible marketplace enrollees received as well as extended Marketplace subsidies to people with incomes above 400% FPL expired and were not renewed by Congress. As a result, out-of-pocket premium payments for Marketplace enrollees have risen 58% on average, making health coverage unaffordable for some individuals. A KFF survey shows that nearly one in ten (9%) of 2025 Marketplace enrollees has become uninsured.

- The ACA set new standards for all individually purchased plans, including plans available through the Marketplace as well as those that existed prior to the ACA. The ACA bars plans from charging women higher premiums than men for the same level of coverage (gender rating) or from disqualifying women from coverage because they had certain pre-existing medical conditions, including pregnancy. All direct purchase plans must also cover certain “essential health benefits” (EHBs) that fall under 10 different categories, including maternity and newborn care, mental health, and preventive care.

Medicaid

The state-federal program for individuals with low-incomes, Medicaid, covered 18% of adult women ages 19 to 64 in 2024, compared to 14% of men. Historically, to qualify for Medicaid, women had to have very low incomes and be in one of Medicaid’s eligibility categories: pregnant, mothers of children 18 and younger, a person with a disability, or over 65. Women who didn’t fall into these categories typically were not eligible regardless of how poor they were. The ACA allowed states to broaden Medicaid eligibility to most individuals with incomes less than 138% of the FPL regardless of their family or disability status, effective January 2014. As of March 2026, 40 states and DC have expanded their Medicaid programs under the ACA.

- Medicaid covers the poorest population of women. Forty-three percent of women with lower incomes (below 200% FPL) and 51% of women living below the federal poverty level (100% FPL) have Medicaid coverage.5

- By federal law, all states must provide Medicaid coverage to pregnant women with incomes up to 133% of the federal poverty level (FPL) through 60 days postpartum. However, in recent years, there has been a growing interest in expanding the length of the postpartum coverage period, and to date, all but one state has opted to take steps to extend postpartum Medicaid coverage to 12 months.

- H.R. 1, the 2025 budget reconciliation law, made significant changes to the Medicaid program. For the first time, Medicaid eligibility for adults in the ACA Medicaid expansion group will be conditioned on meeting work requirements starting January 1, 2027. KFF research shows that most adult women covered by Medicaid meet work requirements or would qualify for one of the law’s exemptions, but many would be at risk of losing coverage because of the administrative burdens related to reporting requirements. The Congressional Budget Office (CBO) estimates that these requirements will reduce federal Medicaid spending by $326 billion over the next 10 years but will also increase the number of uninsured by 5.3 million in 2034.

- Medicaid financed 40% of births in the U.S. in 2024, is a major source of publicly-funded family planning services, and accounts for over half (61%) of all long-term care spending, which is critical for many frail elderly women.

- Under federal law Medicaid coverage of abortion is very limited. The federal Hyde Amendment prohibits federal spending on abortions, except when the pregnancy is a result of rape or incest, or when it jeopardizes the life of the pregnant person. Among the 37 states and DC where the provision of abortion is legal, 17 states and DC follow the Hyde restrictions, while the other 20 states use their own unmatched funds to pay for abortions for Medicaid enrollees who seek abortion in other circumstances.